Andreas Rentz/Getty Images News

Dear readers/followers,

I’m going to be taking another look at Siemens Energy (OTCPK:SMEGF) (OTCPK:SMNEY) here, formerly a part of the great company Siemens (OTCPK:SIEGY). I wrote about Siemens Energy back in late 2022 and managed to catch it at a spectacular low, which resulted in massive comparative outperformance.

Siemens Energy Article (Seeking Alpha)

Unfortunately, my position in this company was rather modest. It was a lift, but nothing noteworthy on a portfolio-wide basis. Still, I know at least one investor who bought heavily into Siemens Energy last year, and this would have resulted in significant outperformance if held onto his shares (which he did).

Let’s revisit Siemens Energy and see what we have here.

Siemens Energy – Revisiting the company and its upside

So. Siemens energy is a fairly easy company to understand. It’s what remains of Gas & Power from Siemens, a company with legacy similarities to General Electric (GE) and similar conglomerates. It also includes a majority stake in Gamesa (OTCPK:GCTAF). In short, you get exposure to pretty much all “things power” that Siemens did, or does.

Competence and know-how are the big arguments here – because the people in charge of Energy know what they’re doing. Christian Bruch has extensive expertise from Siemens, and the former Siemens CEO Joe Kaeser (The “Kaiser”) is the chairman of the supervisory board. Kaeser is the one that oversaw most of what Siemens is today and made sure that the company moved in this direction, which has indeed been a very profitable move for Siemens Energy.

There is a lot to like about Energy has a lot of legacy under its name. The energy division has been a core part of Siemens ever since it became a large business. They have multiple milestones, such as the creation of the Siemens-Schuckertwerke almost 130 years ago, which produced things like aircraft, engines, and trains. It was later bundled into Power Engineering by 1969 and bundled into the Energy Sector in -08 prior to being spun off. Energy is also a huge employer, employing 88,000 people across the world, and its revenues of over €25B means that it’s actually one of the largest segments of Siemens overall.

The Spin-off was performed in 2020, and trading of the Energy shares began around 2 years ago.

When I wrote about it, the performance wasn’t pleasant to behold – it had mostly crashed down and was trading far below par in a market that seemed intent on crushing the stock. The company began trading just above €20/share, and went up to around €30, only to then fall to the current level back in October, having lost almost 50% of its market value for the past 1-2 years.

But that was as low as it went. After that, and I’m happy I held onto the rest given the outperformance we’ve been seeing – but to be clear, selling most of my shares at IPO was really the way to go because I was able to invest substantial capital in “more” attractive businesses which in turn yielded better returns.

Anyway – Siemens Energy today is performing much better, both as a company but also as an investment.

Energy is essentially a play on the current transformation of the industry. It holds things like power generation, grid tech, transformation products for ESG, Wind Energy technologies, and the services to go with all of these segments. Doesn’t sound bad, right?

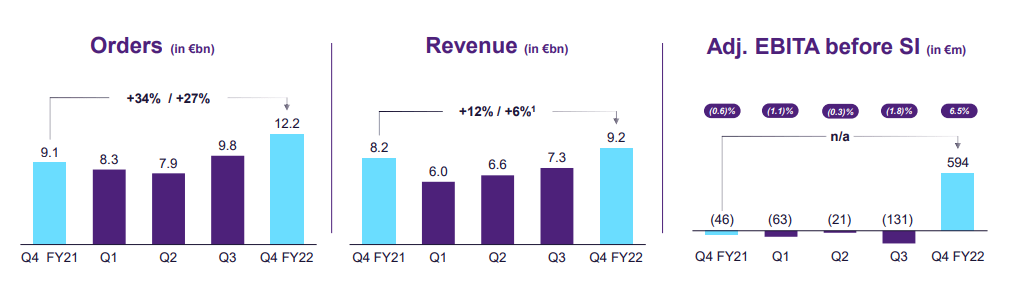

The latest results we have for Siemens Energy are the 4Q22, which ended in November of last year. The new group structure I spoke of in my last article came into effect in late October. The overall financial performance was very good because orders, backlogs, and revenues were decent or at least acceptable. Top line was good, while bottom-line results…

Siemens Energy IR (Siemens Energy IR)

…a dividend suspension can never be called anything except “negative”, no matter the circumstances. Now, to be clear – Siemens Energy is in the midst of a very powerful transformation.

If completed, it should see the company catapulted to the heights of what we can expect in terms of financials.

The company moves from 2022 with its Russia restructuring finished, and with Inflation acts and other tailwinds in the bag. The new reporting structure includes:

- Gas Services

- Grid Technologies

- Transformation of Industry

- SGRE

Gamesa is a real problem for the company, at least in the short term, and challenges are unlikely to go away. Long-term demand is favorable, with wind expected to be doubled by 2022, but production costs, complexities in IT, delays due to SCM, high capacities, and overall production complexities as well as a massive overhead hangover Gamesa as a problem. The company has identified and is taking steps to solve these – with much the same strategies that infrastructure companies in Europe moved in 2016-2018.

Basically, being much more selective on contracts, focusing on price increases and margins, while increasing operating efficiencies. It leads to significant boosts in infrastructure, and I expect it will do similar things here.

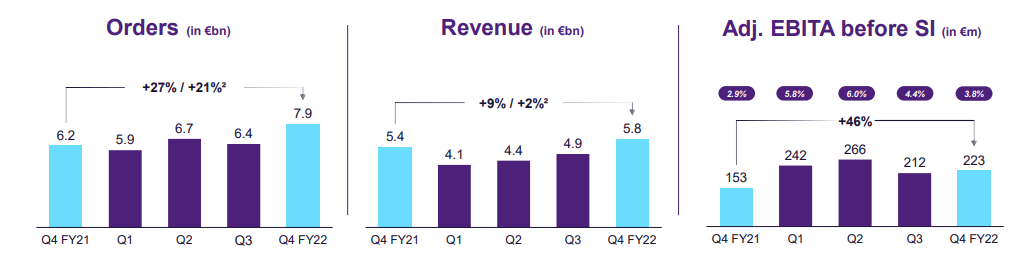

The company did complete and achieve a number of milestones during this past year and the past quarter.

Siemens Energy IR (Siemens Energy IR)

{kind=link}

Siemens Energy plans to delist Siemens Gamesa. The intention is a voluntary cash tender offer, which began in early May of 2022, and is expected to be completed by February of 2023. The company has raised the funds to see this through and there have been no problems on the way – as the tender offer for minority shareholders has been successfully completed.

This will see Gamesa being fully folded into Energy – something that in my view, should have been done from the get-go, rather than listing Gamesa separately.

The company has also seen significant asset sales from Gamesa, which are contributing positively. But the top-line flow is, as I mentioned, a positive one.

Siemens Energy IR (Siemens Energy IR)

{kind=link}

This performance in EBITDA is mostly due to the asset sale – legacy issues held back better performance, and Siemens Energy is still in the midst of that transformation.

However, it’s a company with a close-to-€100B backlog, and a book-to-bill of 1.32. Demand is not the problem. However, I recently wrote about a Hydrogen company in Norway that also has no demand problems – only problems taking that revenue and turning it into profit.

Cash isn’t the company’s problem either. The company has a net positive cash position of close to €3B, even if we take away pension provisions it’s over €2.15B.

Ironically, it’s not the new segments like wind and renewables that do the best – rather, it’s legacy gas & power which is driving the show.

Siemens Energy IR (Siemens Energy IR)

{kind=link}

This segment has most of the backlog, and alone it would drive an annual FCF of €2.4B per year, if not weighed down by the renewables. However, renewables are the future – and once the company gets these in shape, the company should be set to outperform significantly.

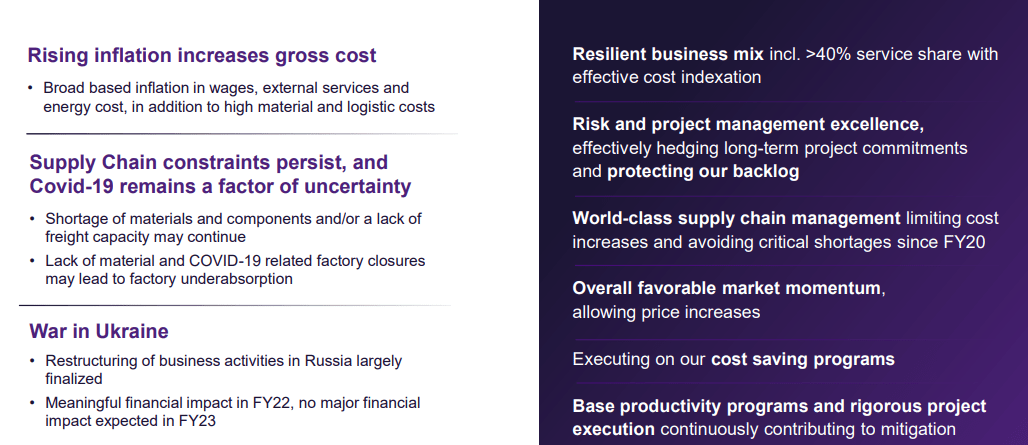

Here’s a good summary of what the company is facing, and what its tailwinds are.

Siemens Energy IR (Siemens Energy IR)

{kind=link}

The net result is a company I’d want to invest in, and own. However, not at any price.

Let’s look at company valuation.

Company Valuation

The valuation for this company remains a tricky business.

Analyst targets for Siemens Energy remain relatively clear – they’ve been declining for about a year but have finally settled around the €20/share mark for the native ticker ENR, similar to my first article on the company. This also represents an upside here, albeit no longer as high as when the company traded below €12/share.

13 analysts follow the company, and 8 of them would suggest that you can now “BUY” the company, with not a single “SELL” rating among the bunch. The worst we get is one “Underperform”. The upside to the €21.68/share price average here is 18.3% at current levels – that’s for the analyst averages.

It remains, however, a question of “how fast” can the company turn things around and start delivering the numbers that we might expect from a Siemens business such as this. With Gamesa folded back into the company and Siemens pushing forward, I expect no less than a 1-2 year period before things can be said to become more positive – so about 2024E-2025E is when I expect real improvements here.

GAAP will likely turn positive in 2023E. For this, you’re currently paying about a 0.35x revenue multiple and a 5x EBITDA multiple. No longer bottom-feeding, as it was during my last article, but still very cheap – though the company also lacks any sort of meaningful dividend here.

Siemens is a forward-looking sort of investment – and I want to repeat, that based on the current thinness of its ADRs, I would only buy the native ticker of ENR traded on the German market. Use a broker that supports these sorts of trades if this is something you want to get into, and if not – be more careful.

Also, Siemens Energy requires years of patience. It’s the sort of investment that might triple, but it demands your patience. If The Company and management get its assets and its portfolio in order, as they seem to be in the process of doing, then this undervalued giant can go places.

So my “dripping” of dividends from Siemens and other German investments have slowly been going into Siemens Energy. I believe the upside for legacy and its portfolio will to a greater degree withstand current troubles due to the energy situation Europe is in – and this is a stance I’ve held since the war started.

The market has, as I pushed in my last piece, now realized how much the company was indeed undervalued, and corrected that to the tune of over 60%. That’s a massive RoR already given the time. You’re paying less than 0.3x to sales and half the book value of the company for what is a superb mix of legacy gas/steam service assets and a class-leading renewable portfolio, even if it’s one that’s in need of a hacksaw.

There remains nothing fundamentally wrong with Siemens Energy beyond the company’s need to improve its margins and be able to work better contracts. It’s BBB-rated, and the dividend is likely restored within the next 2 years.

I can be patient here – and I will be.

My last PT for Siemens Energy was €20/share. I’m not changing it.

Thesis

My thesis for Siemens Energy is as follows:

- The company is one of the more interesting plays in all of Europe on a mix of legacy Gas/power as well as a massive Renewable operation it seeks to pull from the public markets. The company is a transformation play, with a “due date” of 2023-2025 at the earliest, but now is the time to invest.

- I’m going in deeper, and I assign a “BUY” here with a PT of €20/share for the long term.

- Siemens Energy is a “BUY” for me – and I recently bought more.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized)

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

It’s no longer as cheap, but I still believe Siemens Energy to be quite cheap. For that reason, I’m going with a “BUY” here.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.