Thomas Barwick

Co-produced with Treading Softly

What is your retirement dream? Perhaps it’s taking cruises multiple times a year and visiting places you’ve never been. Perhaps it’s traveling the country in an RV and spending countless hours exploring new spots. Or maybe it is simply to spend time with family and loved ones.

Regardless of your dream retirement, there are two constants that will be present – expenses and the need for money to pay them. Very little in life is free and if you want more than the bare basics that nature provides, you’ll have to pony up for it somehow.

I strive to meet my expenses from a reliable and recurring source. This source is the stock market. I created my Income Method to leverage the wealth-generating power of the stock market to create a portfolio of dividend stocks that produce a large sum of income on a recurring basis.

My dream retirement is paid for by the income generated by my portfolio. Namely, it is paid for by dividends from companies that operate all over the United States and abroad. They generate revenue and income, they pay me, and I enjoy my retirement.

Let’s look at two of my holdings which pay me large sums of income, which you may want to pick up shares of for your portfolio.

Let’s dive in.

Pick #1: WPC – Yield 5.2%

Another year and another four dividend hikes from W. P. Carey (WPC) and the good times are just getting started. Real estate is a business that can be a lot like watching paint dry. It is a business where things don’t change quickly.

For an impatient Wall Street that throws trillions back and forth in the blink of an eye, this is seen as a negative. For investors who have the patience to be forward-looking, it can be a source of wonderful income.

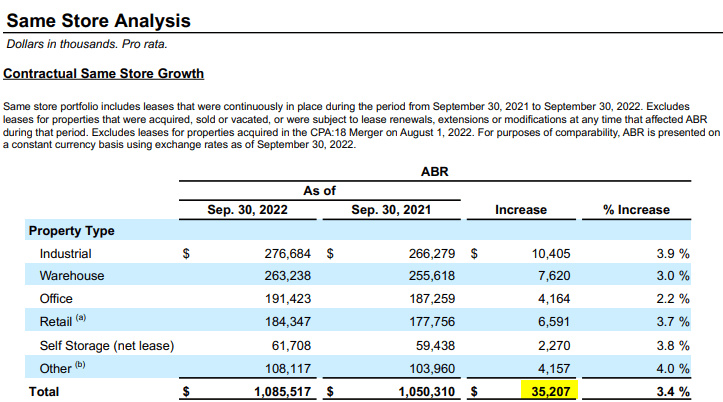

Consider WPC in an environment of high inflation and rising interest rates. Rising interest rates have gradually started having a material impact on WPC’s results. (Source: Q3 Investor Presentation)

{kind=link}

Note that WPC’s same-store growth didn’t skyrocket in a single quarter. In fact, inflation was surging throughout 2021, and it wasn’t even seen in the numbers until Q1 2022, that is how the real estate world works. WPC has leases that are indexed to inflation measures, usually CPI. But you don’t change the rent on your tenant every month! Tenants want some stability. So leases are typically written to reset to inflation once a year.

WPC’s revenue climbs as leases hit their annual update date. The largest chunk of those happen in January – hence why the largest increase in same-store growth occurred in Q1. Some leases might update rent on the anniversary of the lease signing, but the parties can agree to any particular day. For leases that don’t stick to the anniversary of the contract, the beginning of the year is a popular time.

Yet all those renewals in Q1 2022 did not include the impact of the high inflation rates in the first half of 2022 – that inflation will be picked up when leases update again in 2023.

Inflation took a full year before it started showing up in WPC’s numbers, and it will continue to drive revenues higher long after inflation slows down. It will continue to be a strong tailwind for WPC going into 2023.

Let’s talk about the other side – interest rate risk. Wall Street tends to sell off REITs when interest rates are rising. In a way, this makes sense because REITs borrow a lot of money. They tend to use a significant amount of leverage, and interest is WPC’s largest single expense. In Q3, WPC spent $59 million on interest and $22 million on G&A. When the largest expense is increasing, that is something we want to consider as investors.

Yet again, this doesn’t happen overnight. Like much in real estate, interest expense changes slowly, even when the Fed is hiking like a maniac. Why? Because most of WPC’s debt is fixed-rate, and most of it isn’t maturing for several years.

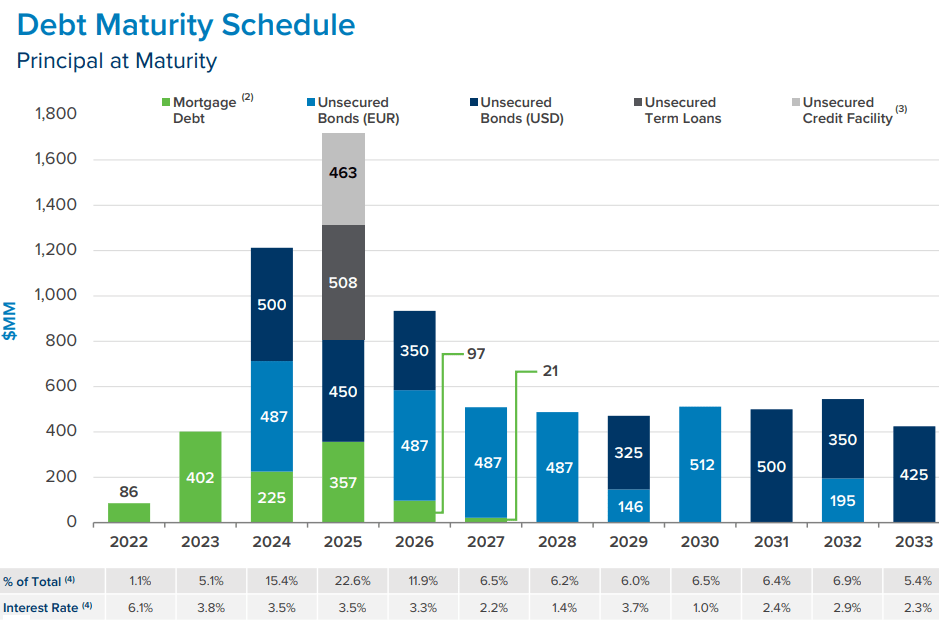

{kind=link}

In 2023, WPC only has $402 million in debt maturing, with property-level mortgages at 3.8%, well above WPC’s average interest rate of 3.0%. WPC doesn’t have to worry about refinancing much until 2024-2026. What will interest rates be by then? We don’t know.

Let’s pretend that interest rates will stay “higher for longer” and WPC refinances all their debt through 2025 at interest rates 400 bps higher. That would be slightly under $3.5 billion – approximately 44% of WPC’s total debt. That would add approximately $35 million per quarter in interest expense gradually over the next three years.

Over the past year, WPC’s revenues increased by $35 million from inflation. (Source)

{kind=link}

In other words, even if interest rates stay high, the expense of higher interest rates has already been offset by rent increases this year. Not to mention that rents will continue increasing at 3% plus next year.

Revenues are rising faster than expenses and will continue to do so for the foreseeable future. If interest rates fall before the end of 2024, something that is a real possibility, then WPC is in the enviable position of eating its cake (enjoying inflation) and having it too (never paying the costs for high-interest rates).

WPC is a time-tested REIT that has survived and thrived through the Dot-Com bust, the Great Financial Crisis, and COVID.

WPC has increased its dividend every year since 1998 and every quarter since 2001. Next year it will join the vaunted “Dividend Aristocrats” list, and it is showing no signs of slowing down!

Pick #2: XFLT – Yield 13.4%

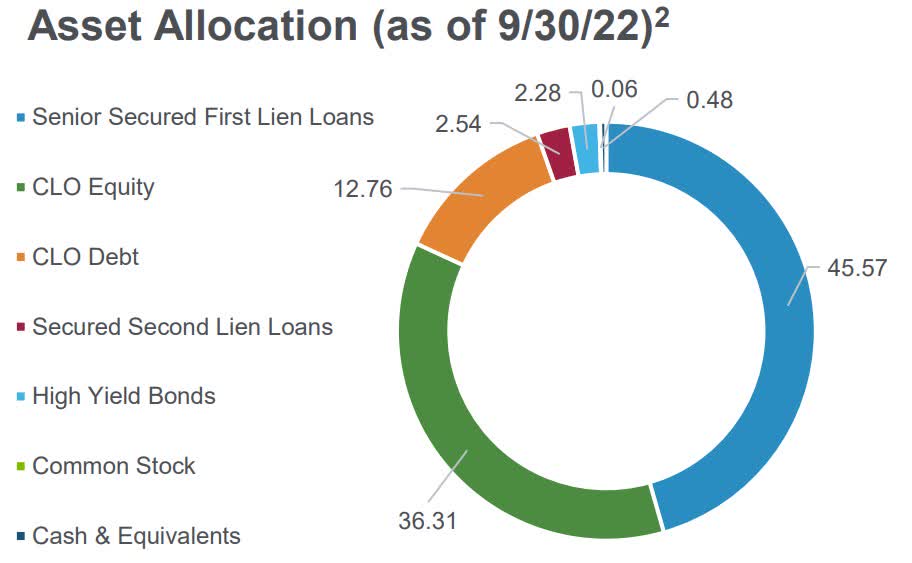

XAI Octagon Floating Rate & Alternative Income Term Trust (XFLT) is a CEF that invests in below-investment-grade corporate debt. It does so through a variety of strategies. In general, XFLT will invest approximately half its portfolio in Senior Secured Loans, and half in CLO debt and equity (collateralized loan obligations) which are an indirect way to invest in leveraged loans. (Source)

{kind=link}

“Leveraged loans” are loans to B/B+ rated corporations. They are “senior secured first lien”, meaning that they are at the top of the capital stack. These loans have a first lien interest on substantially all of the assets of the borrower. If you are reading a 10-Q of a borrower, you will see these loans be reported as “senior secured term loans”.

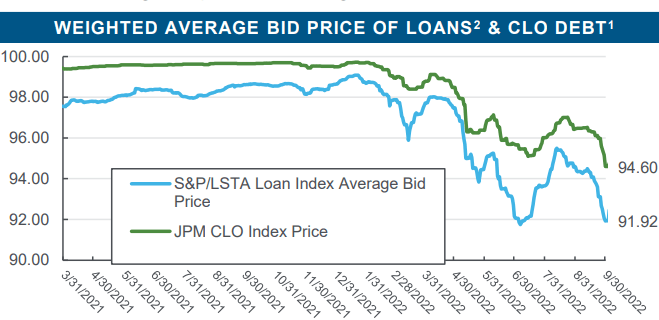

These loans are floating-rate, so the amount of interest borrowers pay rises with interest rates. However, with the Fed hiking aggressively, this has been unable to support loan prices. Loan prices have fallen dramatically year-to-date as large institutions have gone to cash.

{kind=link}

Why would institutions be selling floating-rate debt when interest rates are rising?

Treasuries are more attractive than they were: Many buyers of leveraged loans buy them in an attempt to juice up their yields. They have required returns, and when interest rates were near 0%, there was a lot of incentive to “reach” for yield for insurance companies, banks, and other large institutions. When interest rates are higher, institutions with a very low-risk tolerance will take the opportunity to allocate more capital to the guaranteed returns of Treasuries.

Lowest-risk debt declined in price: It all goes downhill. Treasuries have higher yields and a decline in price, so AAA corporate debt and AAA CLO debt tranches yield more and decline in price.

Here is a look at the prices of CLO debt tranches in Q3:

{kind=link}

As you can see, each step down is to a lower price, which makes sense. Lower-rated tranches should be cheaper.

Fear of recession: Some investors fear a recession and could respond by selling off higher-risk assets. Higher interest rates do put more stress on corporations that have debt, and with credit defaults near 0% last year, they can only go up.

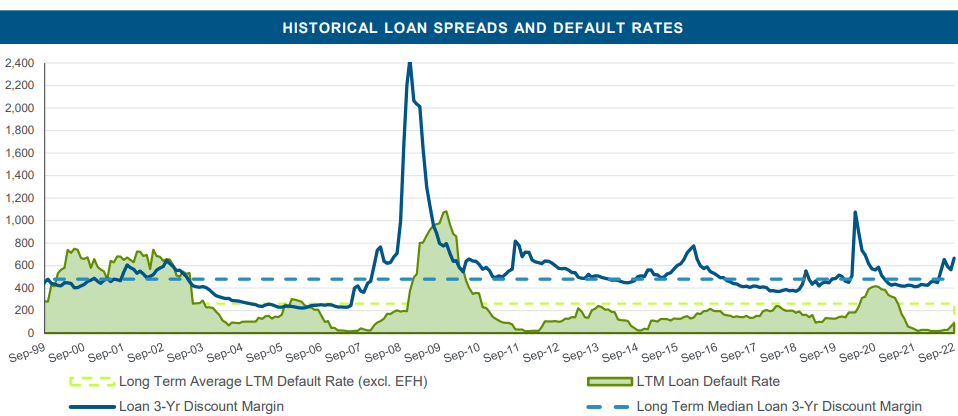

Current loan spreads are on par with levels we have seen when recession fears are high, while the default rate is at historic lows.

{kind=link}

Whenever you are lending money, some borrowers will not pay. That is simply a fact of life. The question as an investor is whether the return you receive will be high enough to make up for the headwind of future defaults. Loan prices are well below long-term averages, and default rates are well below long-term averages.

Note that during the Dot-Com bust, default rates spiked, but the 3-year discount margin (prices) of loans remained relatively stable. The Great Financial Crisis had a much more meaningful impact on loan prices and a more dramatic spike in defaults.

We believe that defaults are likely to remain below average. Corporations are going into 2023 very healthy thanks to spending the time since COVID improving balance sheets.

While rising interest expense is a headwind, most corporations are well-positioned to absorb it having spent 2021 refinancing long-term fixed-rate debt at historically low-interest rates. For many companies, rising interest rates will just be a return to the interest levels they were paying a few years ago.

{kind=link}

We are very bullish on corporate debt and believe it is very underpriced relative to the risk. XFLT has a great balance of direct exposure to loans, and the higher yielding CLOs.

It was XFLT’s exposure to loans that allowed it to recover its dividend much more quickly than peer funds that specialize in CLOs because the cash flow from loans is more stable and is not at risk of being “redirected”. CLO equity positions and junior debt tranches can have their distributions redirected in credit shock events like COVID. In exchange, they have much higher yields. This makes XFLT a very attractive risk/reward option for investors who want to benefit from high yields but want a little bit more security.

{kind=link}

Conclusion

WPC and XFLT both provide my retirement income on a steady and growing basis. WPC pays me quarterly while XFLT rewards me with income monthly. These holdings continue to generate high levels of income, fueling my portfolio.

This way, my retirement planning focuses less on “what can I afford to do” and more on “what would I like to do?”. Financial stress and burdens can be overwhelming and are able to rapidly destroy what otherwise should be the best years of your life.

Don’t let your 2023 be mired by financial stresses and woes, let it be filled with excitement as each dividend arrives in your account and enables you to explore new possibilities that previously were unavailable to you.

That’s the beauty of income investing.