Spencer Platt/Getty Images News

The Industry – The Outlook

I’ve been watching the semiconductor industry since 2020, but missed both the boom and the bust. In 2020, companies like Intel (INTC) looked exceptionally cheap, but I hated the performance of their chips. Advanced Micro Devices (AMD), on the other hand, was seen as a growth machine, but turned out to be more of a bubble.

In a way, semiconductors are a commodity onto their own, driven by the forces of supply and demand. The difference here is, technological edges differentiate companies pitted against each other. Still, margins swing wildly for these companies in a competitive and cyclical industry. The strategy? As Baron Rothschild once said,

“Buy when there’s blood in the streets.”

Thus far, almost nobody in the industry is losing money. But, we’ve seen it happen in 2002, 2009, and 2013:

Taiwan Semiconductor (NYSE:TSM), on the other hand, has maintained its profitability through thick and thin. Even now, as profit margins begin to decline across the industry, TSMC’s profit margins have only increased, displaying the full force of its competitive advantage, a.k.a. moat.

To understand where we are, we have to understand where we’ve been. The years 2020 and 2021 were exceptional years for semiconductors. Profits boomed as the stay-at-home trend boosted the sales of PC’s, smartphones, and tablets. At the same time, consumers were spending like crazy as rock bottom interest rates and stimulus cash sent consumer confidence soaring. With increased demand for the automobile industry’s hottest tech, there wasn’t enough chips to meet the needs of auto manufacturers. All of this boosted sales and margins in the semiconductor industry.

It should come as no surprise that these stocks are now correcting as the market anticipates the next big recession. The question is, “What’s priced in, and what’s not?” Let’s take a look.

The Thesis

I think this was a great buy by Buffett’s Berkshire Hathaway (BRK.B). In the decade ahead, I project returns of 12% per annum for TSMC.

Why Buffett Bought TSMC

TSMC produces over 90% of the world’s most advanced chips. It is my belief that the Chinese, American conflict surrounding Taiwan is really a war over TSMC. Yes, this company is so important to our modern lives that the most powerful nations on earth are risking a war over it.

Now, we may be beginning to see why Warren Buffett’s Berkshire Hathaway recently acquired a stake in the company. Apple (AAPL), which Buffett owns a $100 billion plus stake in, relies heavily on TSMC to manufacture its chips. While Apple gets all the credit for its outstanding iPhones and Macs, it is TSMC’s chips that drive the remarkable performance of these devices. Hint: TSMC has pricing power.

Given the massive profit margins Apple enjoys, there’s lots of room for TSMC to charge Apple a little more for chips, effectively eating into Apple’s profitability. Buffett may be hedging against this outcome. If Apple is too reliant on TSMC, it risks forking over its profits.

I have one more insight into this purchase, and it has to do with fund flows. You see, market-cap-weighted index funds have become very popular over the past five years. The stocks in these indexes benefit from passive inflows. Since buying Apple in 2016, Buffett’s seen the power of inflows from the S&P 500. They’ve sent Apple’s stock soaring. Now, emerging markets appear poised for better returns. I covered this thesis in the article, “Emerging Markets: For The Next 50 Years.” Maybe Charlie Munger and Warren Buffett are seeing potential here as well. TSMC is the largest stock in emerging market indexes, and thus benefits from inflows much like Apple has since 2016.

The Arizona Plants

TSMC’s expanding its production to the United States, building two chip manufacturing plants on American soil. Are the Arizona plants a good investment by TSMC? I’m seeing a few glaring issues with this investment.

Saltwire reported:

“Taiwan chipmaker TSMC plans to build a second chip plant in Arizona and more than triple its initial investment to $40 billion, estimating on Tuesday annual revenue of $10 billion from the plants when they are up and running.”

If we assume a 35% profit margin on that expected revenue, we get just a $3.5 billion profit from the two plants. On the original investment of $40 billion, that’s a pretty poor return on investment or ROA of just 9%. Not great. To put that return into perspective, TSMC currently has a return on assets (ROA) of 19%.

Saltwire also reported:

“The foreign investment by Taiwan Semiconductor Manufacturing Co, the world’s biggest chip contract manufacturer, is one of the largest in U.S. history.

The first chip fabrication facility, or fab, will be operational by 2024, while the second facility nearby will make the most advanced chips currently in production, called “3 nanometer,” by 2026.”

So, one of the largest foreign investments in U.S. history? Yes, the business of manufacturing semiconductors is very capital intensive. But, because it is so expensive to build these plants, there’s also a huge barrier to entry for new competition. This only adds to TSMC’s moat.

Now, the other issue I’m seeing is, does this jeopardize TSMC’s trade secrets? Up to this point, TSMC’s operated solely out of Taiwan. The company’s been known for its secrecy, denying U.S. media from entering its Taiwanese sites. Questioned by CNBC, TSMC employee Tony Chen said “IP [Intellectual Property] protection is very important for this industry, not only for TSMC, but also for the other companies in the industry.”

Now this also begs the question, “Why expand production to the United States in the first place?” Well, as of last year, 60% of TSMC’s customers were U.S. companies. TSMC’s long-term customers, like Apple, want the company to be manufacturing on U.S. soil. This avoids supply chain disruptions and lowers shipping costs. But, at the same time, TSMC will have to pay higher wages and see increased manufacturing costs.

Altogether, this seems like a better deal for consumers than for shareholders of TSMC. TSMC’s pricing power may be partially offset by increased supply from these new U.S. plants. After all, Samsung (OTCPK:SSNLF) also plans to build a $17 billion plant in Texas.

Long-term Returns

To determine TSMC’s future growth, let’s first take a look at the growth of the semiconductor industry. Globally, the industry’s grown a 7.5% per annum over the past 10 years. Meanwhile, TSMC has outgrown the industry at a rate of 14.8%. That’s revenue growth, by the way. Over the next decade, research teams are estimating the market to grow anywhere from 6% per annum to 12% per annum. If you think about all the chips we now need for vehicles, smartphones, computers, military equipment, and AI, this growth is evident. Factor in price increases, and I can see the industry growing at 9% per year through to 2033.

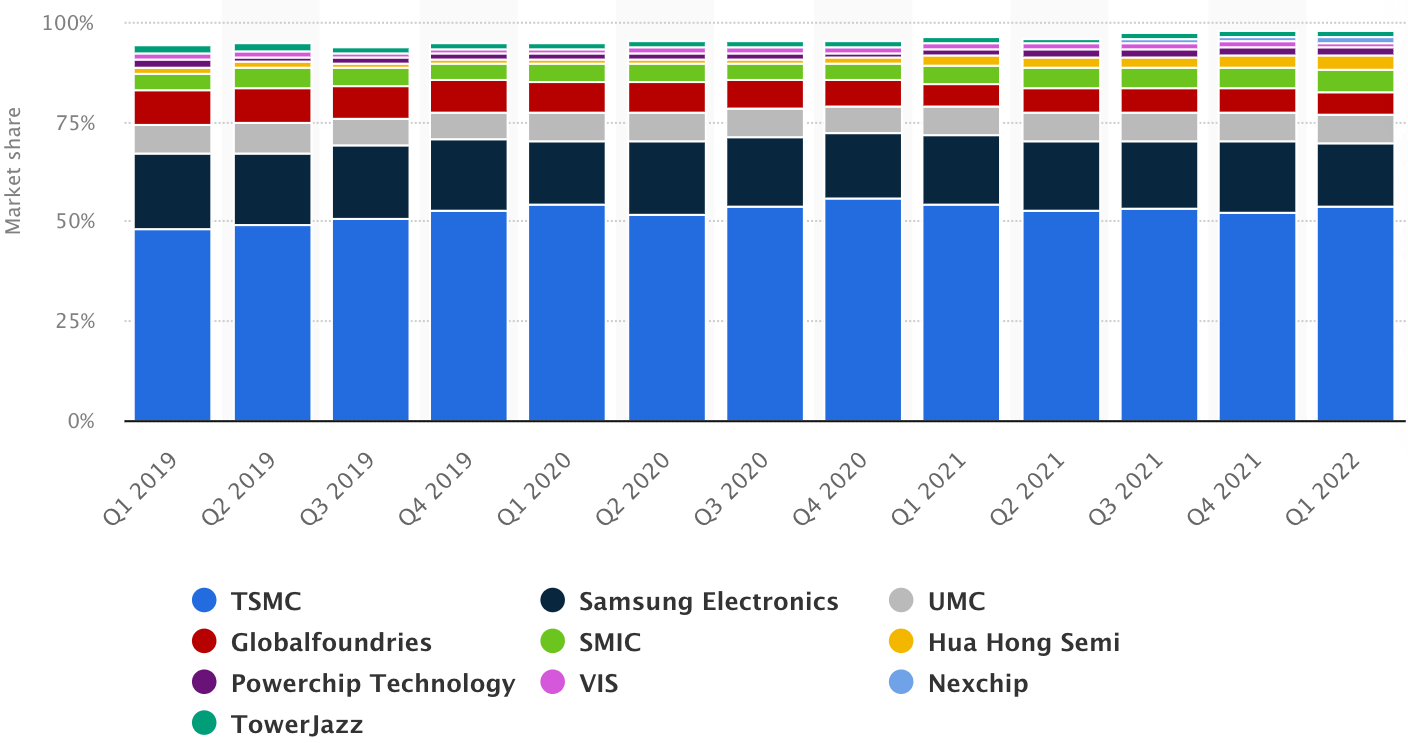

Now, TSMC’s market share appears capped out. Below is an illustration. These are the corporations that actually have fabrication plants and manufacture chips, whereas “fabless” companies like NVIDIA (NVDA) mainly design chips:

Top 10 Semiconductor Companies By Market Share (Visual Capitalist)

TSMC sits on a dominant 53% market share. How did TSMC pull this off? It had singular focus: Manufacturing excellence. When you build the best darn chips the world has ever seen, everything else follows.

Global Semiconductor Foundry Market Share (Statista)

{kind=link}

Assuming TSMC’s moat shines through, the company may be able to maintain its market share. But, the Arizona plants may cause profit margins to decline. Also, keep in mind that TSMC is currently paying a very low corporate tax rate.

My 2033 price target for TSM stock is $185 per share, implying returns of 12% per annum with dividends reinvested.

- I’m estimating TSMC can grow its EPS at a rate of 7% per annum from $5.89 today to $11.60 by 2033. I’ve applied a terminal multiple of 16x. Because TSMC doesn’t buy back stock, the company should be able to grow its dividend at 11% per annum.

In Conclusion

TSMC is one of the world’s premier dividend growth stocks. The tailwinds and the moat are undeniable. That said, I would caution that TSMC’s plants in Arizona may hurt the company’s profitability metrics, and that the semiconductor industry can be quite cyclical. Buffett may be hedging his Apple position with this purchase, and the buy is also a bullish sign for emerging market indexes. I rate TSMC as a “buy” here, and if it falls much further, I’d upgrade it to a “strong buy.” Will you be following Buffett into TSMC?

Until next time, happy investing.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.