Roman Stasiuk

Dear Readers/Followers,

So, yeah. Polaris (NYSE:PII). This is a company that was on many dividend investors’ radars in both -21 and -22 as the demand for these skyrocketed similar to other cyclical ones that I did follow closer, such as THOR (THO). It’s a common theme that investors may believe there will be a massive bounce – and sometimes, indeed, there is.

However, I was dubious – and I don’t invest in bounce-ups in any case, so I stayed conservative about Polaris. This paid off, because Polaris didn’t really outperform the market in 2022.

Let’s look at what Polaris may offer you.

Polaris – What does the company do?

Polaris has been around for over 50 years, and its first focus was the creation of snowmobiles, with the first models going around 20 mph and weighing half a tonne or 1000 lbs. The company’s product quickly gained traction though, and the people involved in the founding of Polaris are also (one of them) involved in the competing company Arctic Cat today, though PII has obviously done somewhat better for itself.

Polaris expanded its product range to include smaller, consumer-sized snowmobiles. In the ’80s, it moved into ATVs and later moved into On-road vehicles, and BEV products, and finds us where the company is today – producing both on-road, off-road and in-between vehicles, the platforms are which are used in applications from police, to firefighting, to patrols, to forest and winter applications. The company is even active in the defense industry with the MRZR platform, which is used by the U.S. Marine Corps, a vehicle with a very limited size that can run on JP-8 (Jet fuel) and can fit into an Osprey VTOL.

The company builds impressive vehicles for impressive applications. It’s a company with a $6B market cap. The company has no investment-grade credit worth mentioning – the closest it has are Ba3 ratings on its revolvers, and this does not qualify.

Author’s Photo (Author’s Photo)

{kind=link}

Now, working where I work (at this time) about 150 miles north of the polar circle, Polaris vehicles are a common sight (almost more common than cars during 1-2 meters of snow as we’re having now) – both snowmobiles as well as ATVs. Everyone has at least one snowmobile. I don’t drive them daily, but I do drive them, and a colleague of mine has an ARO 3 Timbersled that is, pardon my language, fun as hell.

So I’m not exactly unfamiliar with the company or its products.

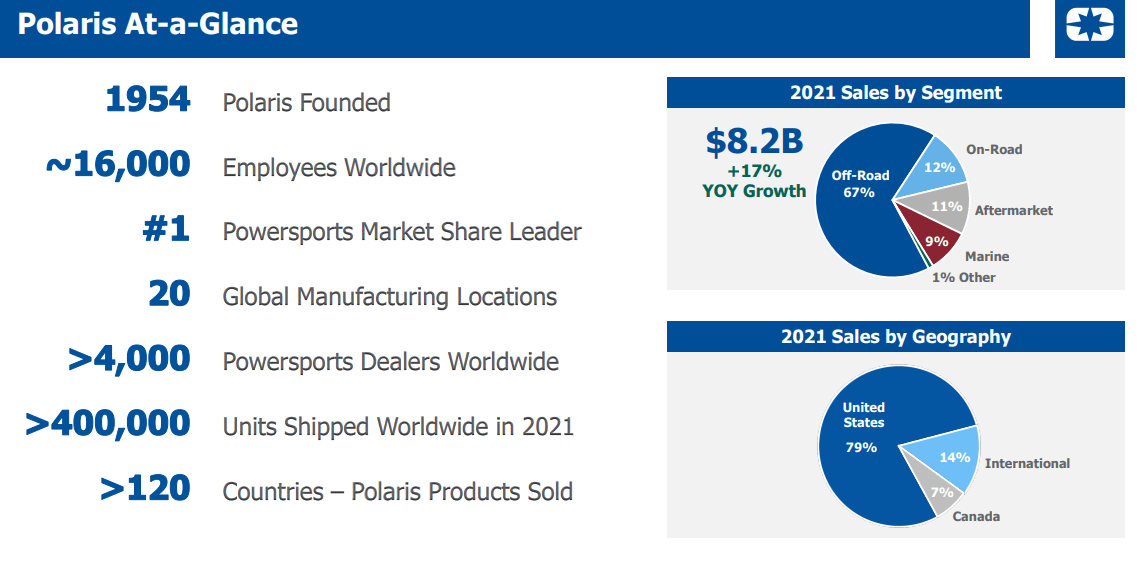

Polaris is an absolute market leader.

{kind=link}

And while there are competitors in most of its field, and some people here drive Yamaha’s or other brands, Polaris is really the brand most people “want” (if they can afford it).

The company generates impressive amounts of sales, and leaves its competition far behind, outperforming in Powersports retail by a sales factor of 2x. Polaris has the scale advantage, brand presence, manufacturing advantages, sourcing advantages, and distribution to retain this position unless something drastically changes.

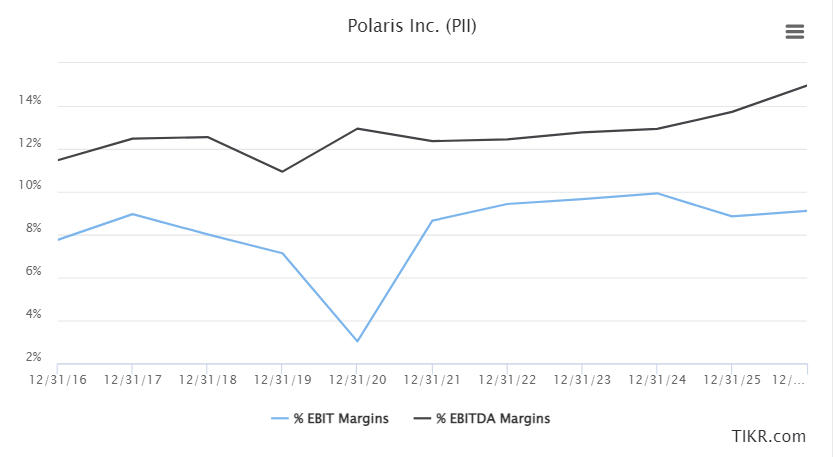

I’ve looked at Polaris before – quite a few times actually, and was impressed with their margins, both the gross and operating level, given what they essentially produce are vehicles – and vehicles/cars aren’t exactly known for being conducive to having great margins. PII shows impressive numbers still.

{kind=link}

As it stands, the market took major beatings in 2020, and still haven’t fully recovered, but for the next few years are expected to be at least stable when looking at a high sort of picture. That 8% in terms of pre-tax is sort of where the company seems to land.

{kind=link}

However, like any vehicle or motor company, PII is primarily a play on cyclical discretionary products. That means its exposure to input, to macro risks, to supply chain risks, to recessions – is high.

This is the main reason why despite PII being cheap (because it is cheap, more on that later), I have elected to stay out of this investment because I have learned what exactly recessions can mean for highly specialized consumer discretionary companies when supply chains break down. This is not even mentioning the risk of recalls (which the company recently faced).

Moving into a more conservative economic reality, luxury premium products, which is what Polaris represents, are likely to face slowing sales and issues bringing products from distribution to sales.

As of yet, the company hasn’t seen any lower demand for its products – but it also hasn’t been able to fill orders, due to supply chain restraints. This is absolutely key – Polaris would have to capitalize on this demand prior to an eventual recession hits, because if/when that hits, things are bound to go down south – and that includes demand. At that point, it won’t matter how high inventories are, because people won’t want to be buying as much.

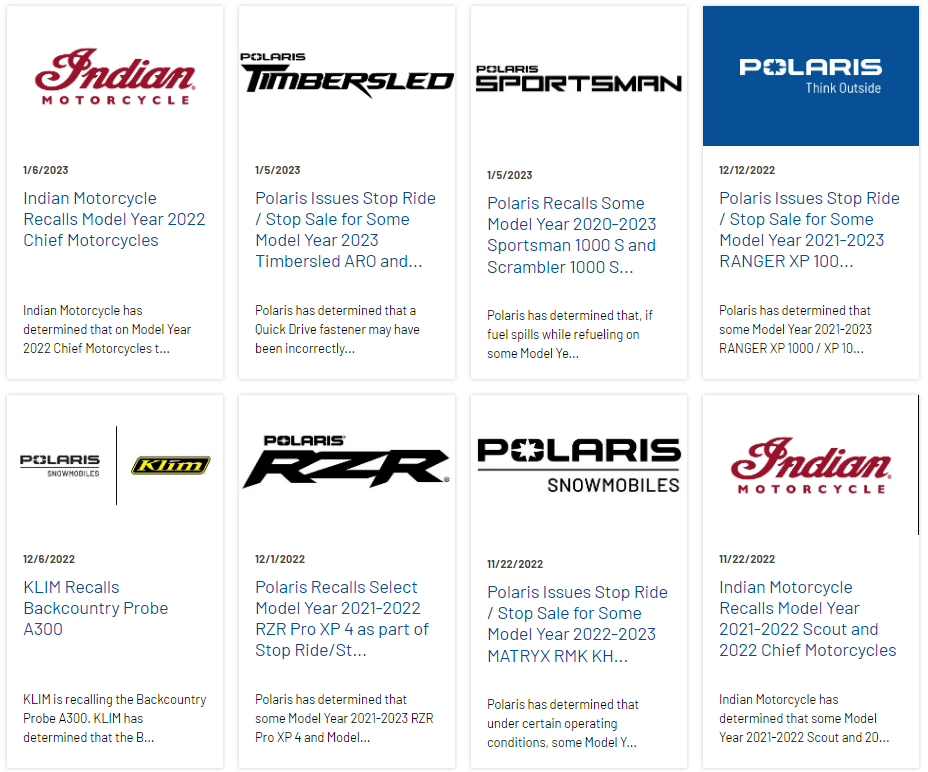

These trends are what we need to discount for – and these trends are what the market seems to discount for. It’s not as though product recalls seem rare for this company.

Polaris Recalls November-january (Polaris)

{kind=link}

To be clear, I think the company is an excellent, innovative, qualitative producer of quality products. Despite its lack of a credit rating, I view its fundamentals as solid, and it has a good earnings trend.

It’s the market leader, and it has good manufacturing, sourcing, and sales capacity. But that doesn’t make it immune to macro, and it certainly doesn’t make it immune to mistakes. And that’s what I believe is preventing Polaris from outperforming as an investment, both in the short and likely in the medium term as well.

3Q22 did nothing to alter my perception here. The company saw a massive 32% sales increase, its margins solid at the EBITDA and gross levels, and an impressive increase in EPS followed by an increase in guidance. Demand indications were strong.

{kind=link}

However, dealer inventory levels and manufacturing is what we need to look at here. My assumption is the following. We’re looking at a recessionary sort of environment in 2023, which could negatively influence demand for PII. If this happens, manufacturing and inventory won’t matter, because the customers are no longer there. While the company continues to innovate with new products…

{kind=link}

…this really won’t matter if basic fundamentals for demand aren’t there anymore, such as fear of, or an actual recession. For the time being, Polaris is playing the cost game very efficiently. They’re raising prices to offset for expenses, and so far people are accepting the increased premium – over in Sweden as well. If you have the money, you want a Polaris – and if I stay here for an extended period of time due to work, it’s like I will buy one for myself as well.

But given my income and discretionary spending availability, I’m hardly the typical PII customer – most others I speak to consider other brands as the economy grows worse and worse – or simply don’t buy at all.

I can’t characterize 3Q22 as anything other than a success for Polaris. FCF was up significantly, and the company’s operational cash flow is impressive. Here is the current full-year guidance from the company.

{kind=link}

And in many ways, I agree with what the company sees. I believe supply chain challenges will continue to ease, I believe inventory levels are slowly resetting, and I believe pricing actions will see margins improve.

However, none of that matters as much, when the main impact for consumer cyclical is bound to be demand, which could see the company fail to rise or perform as well as could be expected as an investment.

Let’s look at where the valuation currently stands.

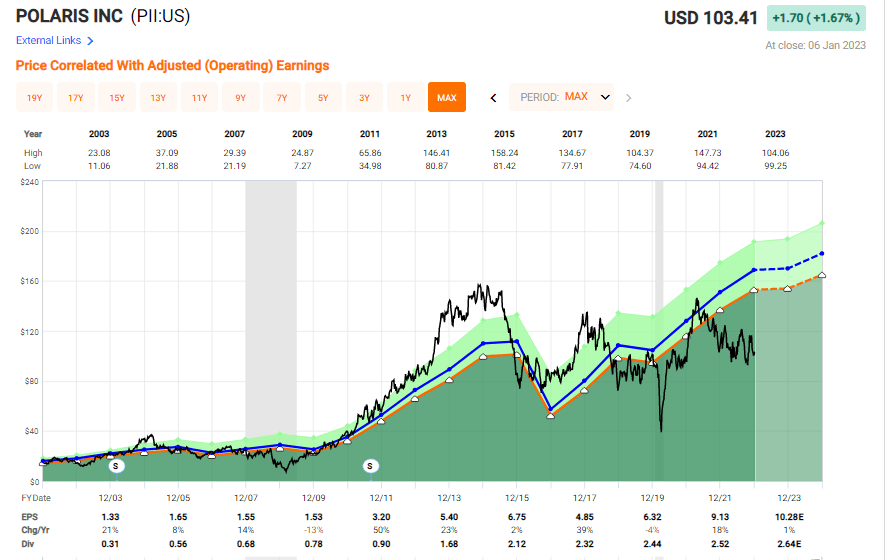

Polaris Valuation

Polaris is one of those companies that has been in the doldrums for a number of years now. To give you a quick implication of where this section is going, I believe that Polaris is a “BUY” here, but I believe it may be some time before you see realization of that upside that’s implied from earnings and historicals.

F.A.S.T Graphs Polaris Valuation (F.A.S.T graphs)

{kind=link}

The company shows every indication of being your very classic cyclical business, with extreme ups followed by extreme downs. It makes it clear when we should be buying, and when not. Now is a time that we should show interest in Polaris, but the current set of fundamentals (macro) also means that we should be aware, and careful.

There’s a reason consumer cyclical is probably my least favored investment sector for 2023. These cyclical can stay down in the dumps for years – and we don’t yet know what the next couple of years will bring. I’d rather invest in an undervalued utility providing gas and heat/electricity, than a leisure company that, frankly, people don’t really need all that often.

However, it’s only fair to say that Polaris at this time is undervalued. Even just assuming a 14-15x P/E, and ignoring that premium, you’d still get annualized 28.5% until 2024E, if we see normalization.

The company has been undercovered since October, which is pretty interesting to me – because now is really the time when investors should be looking at Polaris more – not while it was riding higher on trends from 2020-2021.

Yes, margins are still lower than in historical years – but that’s not the main thing. If you’re focusing on margins, manufacturing, or supply chains here, I believe you’re close to, but perhaps missing at least part of the point. Focus on macro and demand – that tells the story for 2023-2024.

And that story is problematic.

In its peers, we can compare Polaris to Leisure products. In this peer, we find BRP (CA:DOO), and we find Brunswick (BC). Both of these companies are currently cheaper than Polaris – in the case of BC, substantially cheaper.

So being cheap in the midst of a cyclic downturn really isn’t a massive argument for this business. It’s a requirement/standard set of circumstances. We could also compare it to automobiles, but that’s not as relevant as I see it, and it colors the peer comparison somewhat.

Street targets are positive. 15 analysts follow PII, giving it a range starting at $81/share and going up to $175, basically the difference between night and day. Analysts are almost split down the middle – 7 are at “BUY”, the rest more or less at “HOLD”/Underperform. So understanding why the company trades as it does isn’t really that complicated here.

Polaris valuation is a reflection of the uncertainty in the current market estimates for the period of 2023-2025. I believe that period is unlikely to go away soon.

Based on these circumstances, I discount PII heavily, and would not go higher than 10-11x P/E here, which caps PII at a normalized PT of $115 per share. That’s a “BUY”, but a conservative one. The analyst average is around $5 higher at ~$120.

However, the company could go either way – which is why the following is my thesis for the common, and why I would point you to options instead.

Thesis for the common share

- Polaris is a world-leading play on ATVs, snowmobiles, and interesting, necessary alternative modes of transportation. It’s a cyclical stock that’s seen share price pressure for years going into COVID-19 and these recessionary trends we’re currently facing.

- While the company is attractively priced and I give it a conservative price target of $115, I consider it a better choice to consider some of the options for investing here.

- Still, Polaris is a “BUY” here.

Remember, I’m all about :1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The Options Thesis

I would consider it a better choice to play the safe card here by going for cash-secured PUTs. I found the following available, though markets are currently closed.

Polaris PUT option (Author’s Data)

I believe the annualized RoR here, together with the potential of buying at below $90/share for a yield of close 3%, to be far better than investing here. I don’t believe we’re bound for a massive uptick in the business.

I may write this option if come market open the premiums remain.