wildpixel

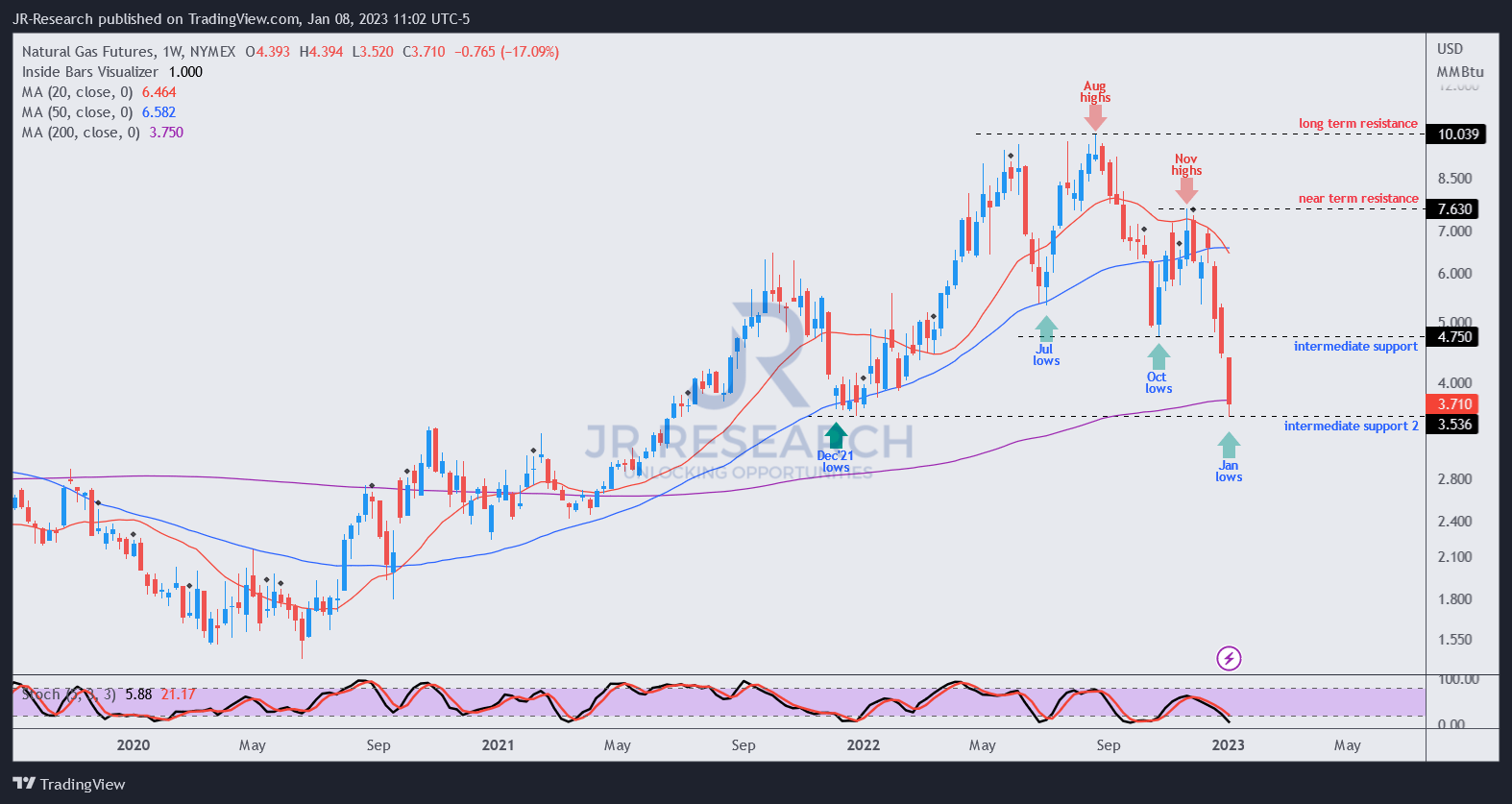

Black Stone Minerals, L.P. (NYSE:BSM) operates a portfolio of oil and natural gas mineral assets. The collapse of natural gas futures over the past few months has also placed BSM in an interesting position for investors. Even though NYMEX natural gas futures (NG1:COM) have declined nearly 65% from their August highs, BSM’s hedges have likely helped it to avoid significant damage.

Accordingly, Black Stone Minerals reported in its Q3 filings that 98% of its oil and condensate and 72% of natural gas production for 2022 had been hedged. Therefore, we believe that it helps provide significant clarity over the company’s distributable cash flows (DCF), which are critical to sustaining its robust dividend yields.

Despite that, BSM is not immune to the underlying energy market volatility. As such, it has also fallen nearly 25% from its November highs (in price-performance terms).

Still, it has been a much better performance against the futures market, suggesting that management’s execution of its hedges moving forward could be crucial.

Management clarified that it had secured hedges on 66% of its oil and condensate volume for 2023. It had also hedged 65% of its natural gas volume for 2023. Furthermore, its hedging position for 2023 has improved significantly relative to 2022, with its oil swap contract price for Q1’23 nearly 20% higher than its Q4’22 price. In addition, its natural gas swap price for Q1’23 is almost 37% above the current strip.

BSM price chart (weekly) (TradingView)

{kind=link}

Our analysis suggests that natural gas futures are at a critical juncture. We expect a near-term rebound in NG1 over the next few weeks, which could determine the medium-term trend bias for natural gas futures. Hence, we encourage investors to refrain from using the current strip as a benchmark to assess the potential derivatives gains predicated on BSM’s Q1’23 swap pricing.

Black Stone Minerals reported a swap price of $5.07 for Q1’23, hedging a volume of 9M MMBtu. While it has a higher swap price of $5.15 for Q2’23, the hedging volume is nearly 10% lesser.

We believe the position is appropriate as a recovery toward the $5-$6 region in H1’23 is possible after such an extended and steep selloff. However, investors should understand that natural gas futures are highly volatile and are incredibly challenging to predict with absolute certainty. Despite that, the technical signals are pointing to a bounce. Therefore, the 37% against the current strip is expected to narrow significantly if our thesis plays out.

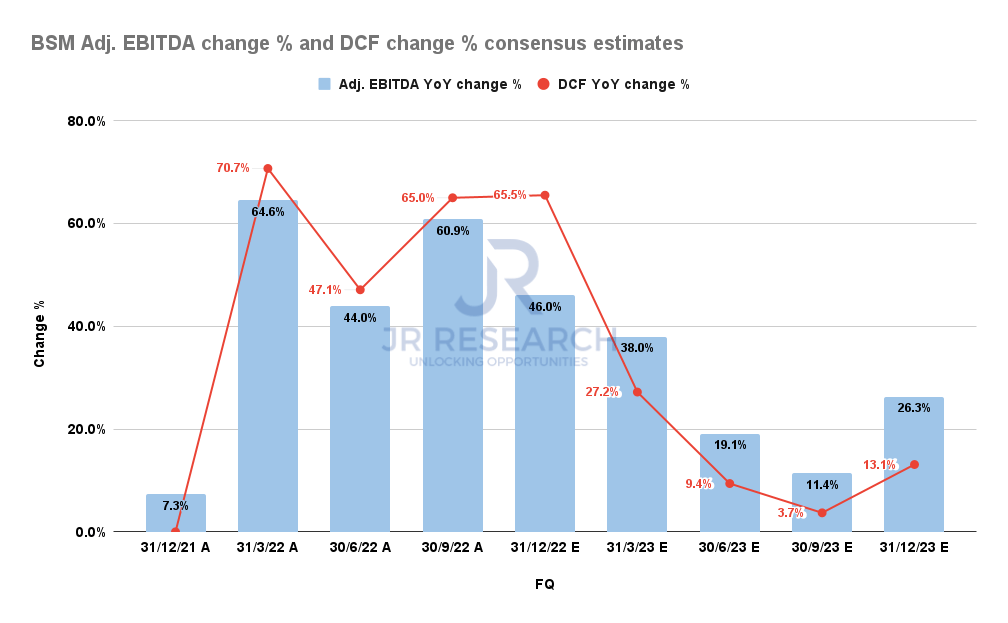

BSM Adjusted EBITDA change % and DCF change % consensus estimates (S&P Cap IQ)

{kind=link}

The revised consensus estimates still project a growth normalization in H1’23 before recovery from H2. Hence, investors need to assess whether the recovery in energy prices could sustain from H2’23, particularly for natural gas futures.

While the headwinds against the natural gas market have intensified lately, we believe that it has likely been reflected in the collapse over the past few months. For now, Black Stone Minerals has yet to hedge its volumes for 2024, which could imply that the company is confident of a medium-term recovery.

Citi (C) remains constructive, postulating that “eyes will turn to the build for next winter.” China’s LNG demand could increase following its reintegration with the world as it exited its harsh COVID lockdowns, potentially reclaiming its throne as the world’s leading LNG importer from Japan.

Still, a further fall in natural gas prices should not be ruled out, which could batter BSM further (despite its hedges, as it’s not immune).

Hence, the critical question is whether the current opportunity is attractive enough.

BSM last traded at an NTM dividend yield of nearly 13%, close to the two standard deviation zone over its 10Y average. Hence, the market likely sees significant risks in its operating performance, as BSM was not re-rated in 2022.

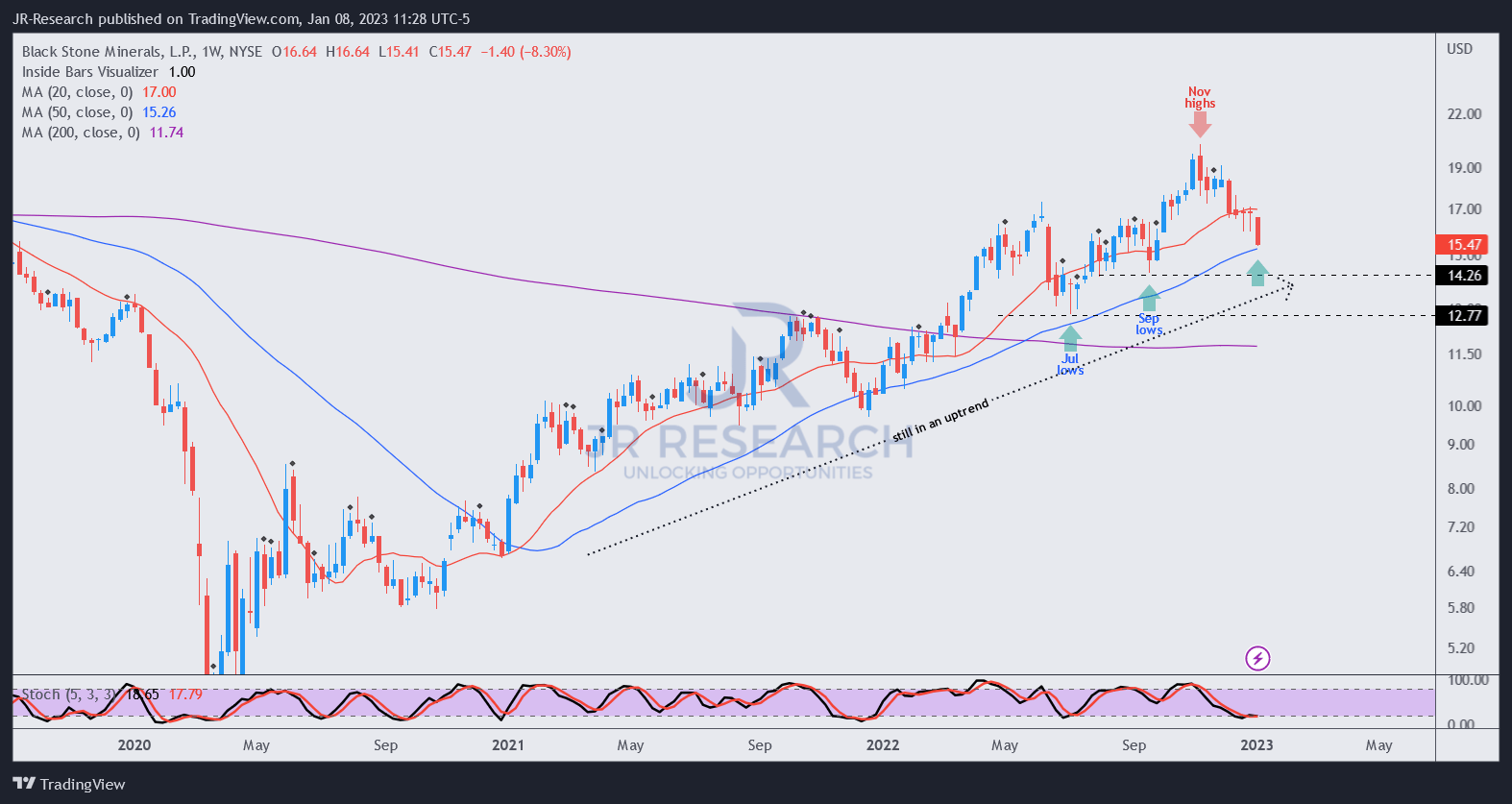

BSM price chart (weekly) (TradingView)

{kind=link}

Notwithstanding, we see a buyable bottom as BSM has pulled back to its 50-week moving average (blue line), which has undergirded its recovery from its COVID lows.

However, we see some ominous price action signals on its longer-term monthly chart, suggesting investors need to be cautious about “holding the bag” if the recovery fails to pan out.

Therefore, while we assessed the current opportunity as a buyable bottom, investors should be ready to cut exposure if BSM falls decisively below its 50-week moving average. Accordingly, it could represent a significant change in trend, suggesting that market operators could be anticipating further downside moving ahead before an eventual bottom.

Rating: Cautious Buy.

Note: As with our cautious/speculative ratings, investors must consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.