bunhill

Devon Energy Corporation (NYSE:DVN) stock has continued to collapse, given the recent battering in the underlying markets. Investors have turned increasingly cautious about near-term demand/supply dynamics in the energy markets.

DVN has declined nearly 20% since our Sell article, as it underperformed the S&P 500’s (SPX) (SPY) 1.7% gain.

Therefore, despite its relative undervaluation to the SPX, some weaker DVN bulls who bought its October highs could have been forced to flee, as we could potentially enter a global recession.

While we kept a Hold rating in our previous update, we believe an opportunity may have arisen even for energy bears sitting on the sidelines.

Two critical changes have occurred since our update in early December. First, China has already reopened from its COVID lockdowns in a hurry, even as several countries have recommended restrictions on Chinese visitors.

However, the rapid reopening moves have also led to a resurgence in COVID infection, causing supply chains to be disrupted and impacting economic activity across industries. It has also affected its labor supply, as workers reported being sick from COVID infections, impacting industrial activity.

However, analysts have also prognosticated that the peak of China’s COVID wave could occur in late January, coinciding with its Chinese New Year festivities. As such, we could be mere weeks away from a recovery in consumption and industrial activity, which should lift the demand for energy and commodities.

Despite that, WTI crude oil futures (CL1:COM) have continued to struggle to recover their bullish bias, as investors likely feared China’s recovery might not be adequate to address global recessionary headwinds. NYMEX natural gas futures (NG1:COM) have also collapsed to their December 2021 lows, effectively giving up all its gains for 2022. Warmer-than-expected weather has added more oversupply concerns to the NG1 market dynamics, as investors are likely satisfied that Europe could sustain itself with its current storage capacity.

Hence, it has been a remarkable reset for energy markets, even though WTI crude oil futures remain well above the critical $60 region. Therefore, buyers have resolutely defended the current levels, seeing a potential recovery from China as a critical tailwind for oil and gas recovery.

Moreover, the recent release of the US employment figures suggests that wage growth has slowed markedly. Notably, US average hourly earnings increased by 0.3% MoM in December, coming in below the consensus estimates.

As such, investors are likely assessing whether there could be an earlier pivot from the Fed, even though its recent minutes from its December FOMC suggest otherwise. Notably, an earlier Fed pivot could strengthen the bullish thesis of no recession or mild-to-moderate recession, softening the blow from potential demand destruction in Europe, which could already be in a recession.

Therefore, we urge Devon Energy investors to pay close attention to the macroeconomic developments, as we believe these factors could impact the directional bias for DVN in the near- and medium-term.

Notwithstanding, Devon Energy is still slated to report a record year in FY22, with the company expected to post revenue of over $20B (up 64% YoY). However, we believe investors are likely already looking ahead.

As such, it could explain why DVN is down nearly 20% from its October highs as market operators parse its FY23 outlook. It’s critical to note that industry analysts have also revised their earnings estimates further downward in December for Devon and its peers, likely baking in worse macro risks.

However, Devon is still projected to post a solid performance in 2023, with revenue growth expected to be flat YoY, while adjusted EBTIDA is expected to fall by just 2.2%. Hence, we assess that the bar is still set at a relatively high level for Devon to cross, increasing execution risks for the company if macro headwinds intensify further.

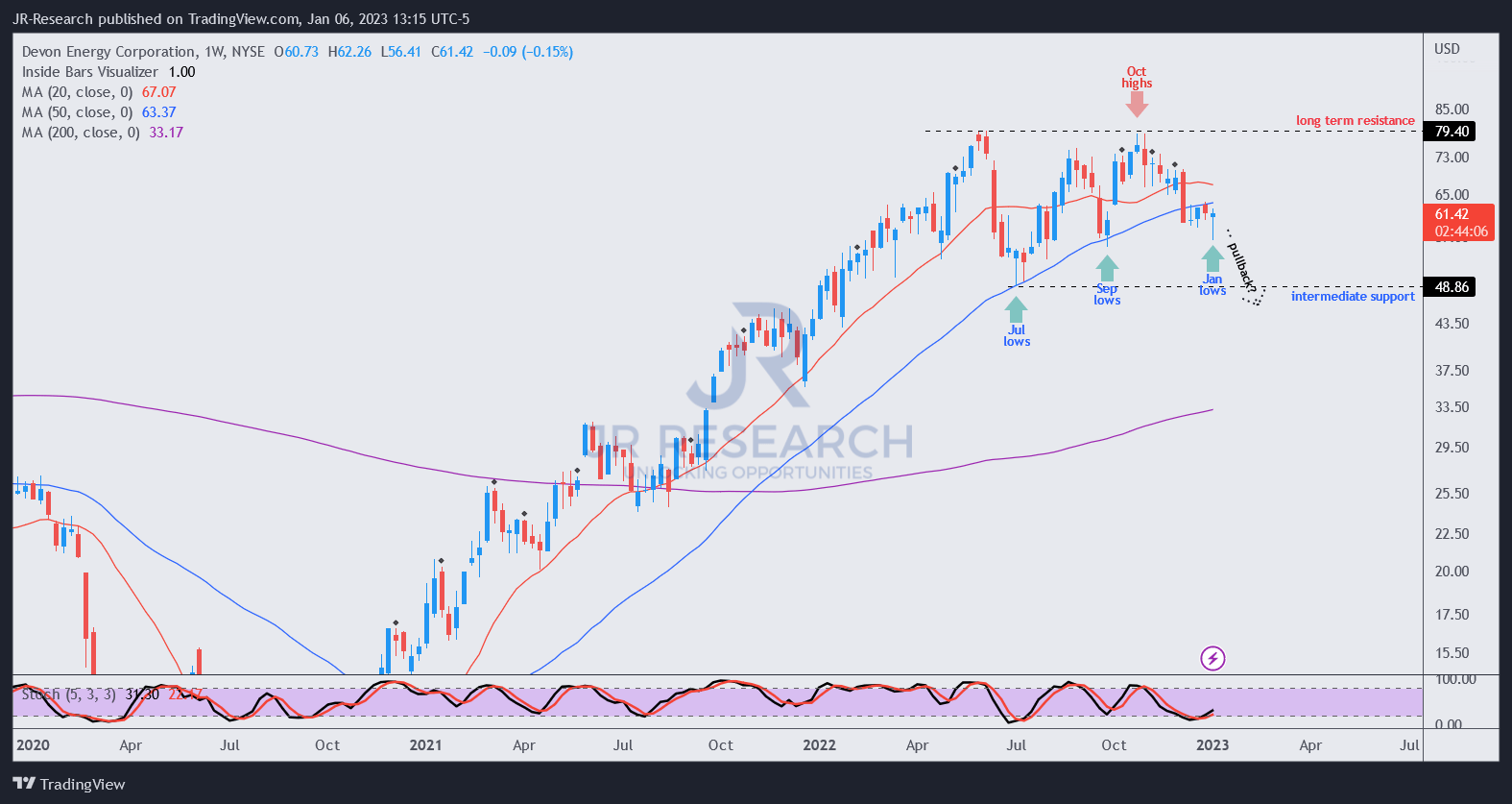

DVN price chart (weekly) (TradingView)

{kind=link}

Notwithstanding, we gleaned a potential buyable dip on its medium-term chart, suggesting that investors can consider adding exposure at the current levels. The underpinning thesis of no/mild recession and a faster-than-expected recovery from China is critical in lifting buying sentiments.

However, investors should also note that DVN’s price action is at a critical juncture. If it fails to regain the support of its 50-week moving average (blue line), it could imply that market operators deem further downside risks as appropriate in its operating performance. As such, investors should be cautious and consider cutting exposure partially or fully.

Rating: Speculative Buy (Revise from Hold) with a price target of $70.

Note: As with our speculative ratings, investors must consider appropriate risk management strategies, including pre-defined stop-loss/profit-taking targets, within an appropriate risk exposure.