YinYang

The December jobs data suggests the Fed’s path to higher rates remains on track. The latest jobs data showed that the unemployment rate sank to 3.5% due to more than 700,000 jobs created on the household survey. Meanwhile, the non-farm payroll grew by 223,000 vs. estimates of 203,000. Additionally, average wages rose by 4.6%, which was weaker than estimates of 5.0%.

ISM Disaster

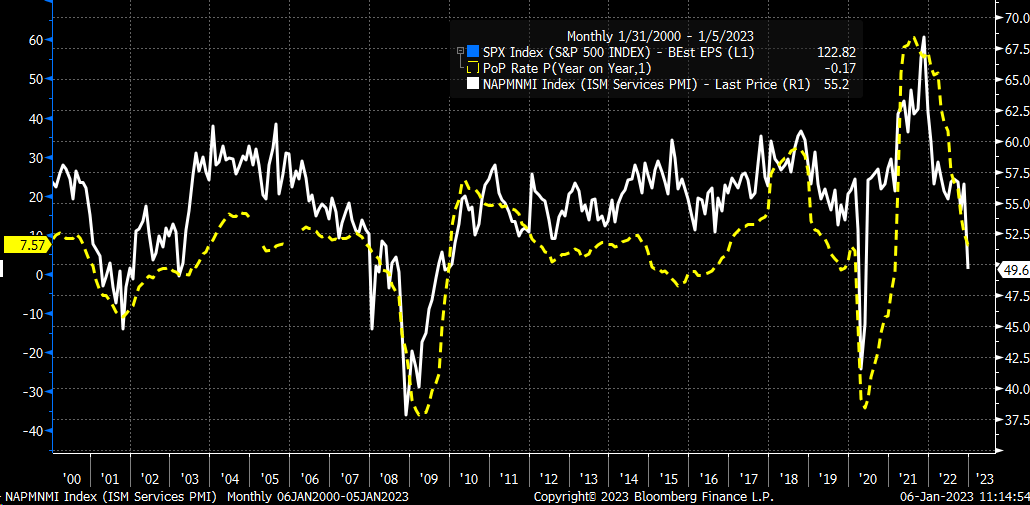

However, that solid data point has been overshadowed by a weak ISM services data point, which suggests the sector slipped into contraction in December. Whether or not December is a one-month outlier or a sign that the economy is slipping into a recession is unknown. But the market is reacting strongly to the weaker-than-expected ISM services reading.

The ISM services index fell to 49.6, well below estimates of 55, and last month’s reading of 56.5. If this turns out to be correct, then it suggests the economy slowed materially in December. It’s easily overshadowing the December job report.

The equity market is rallying because the weak ISM data has dramatically weakened rates and the dollar. However, if it’s the case that the service sector is slipping as the ISM data suggests, then that’s horrible news for equities longer term because it will result in even lower earnings revisions.

{kind=link}

Bloomberg

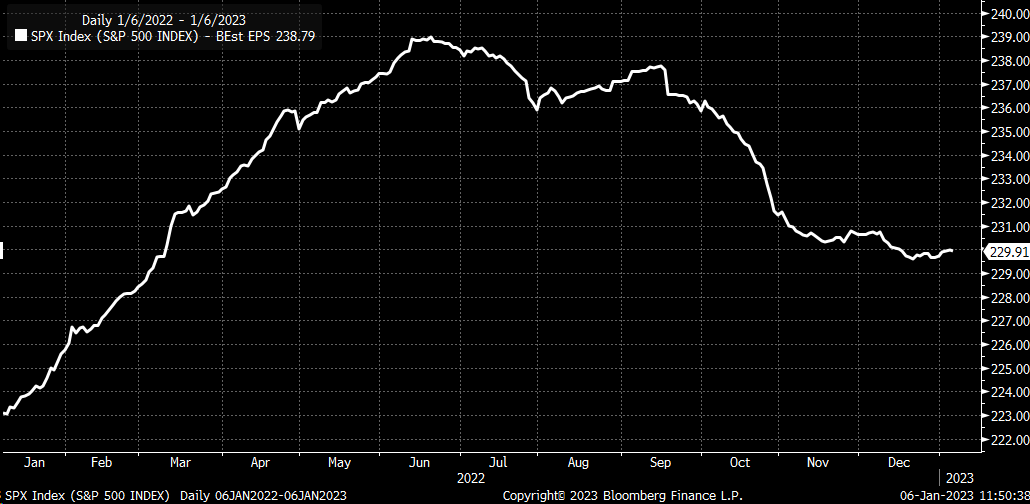

Earnings estimates for the S&P 500 have been falling pretty steadily, and if the service sector’s weakness is correct, it calls for even more downward earnings revisions. Blended earnings estimates for the S&P 500 over the next 12 months have fallen to $229.91 per share and, based on today’s ISM data, probably have much further to drop.

{kind=link}

Bloomberg

Is Bad News Still Good News?

At this point, the equity market seems to think the bad news is good news because it means the Fed will stop raising rates. The problem with this mindset is that the Fed has already gone past the point of no return, and there’s hardly enough time left to stop the Fed from getting to within striking distance of its 5% rate. The more bad news we get on the economy, the worse it will be for the equity market. Because one way or another, the Fed is getting to the point where it’s almost finished raising rates.

So at this point, pausing rate hikes isn’t going to be enough to reverse the damage to the economy if that is the case. Today’s labor market data suggests the job market is holding up quite well and that the Fed’s policy is working to slow hiring without causing massive layoffs.

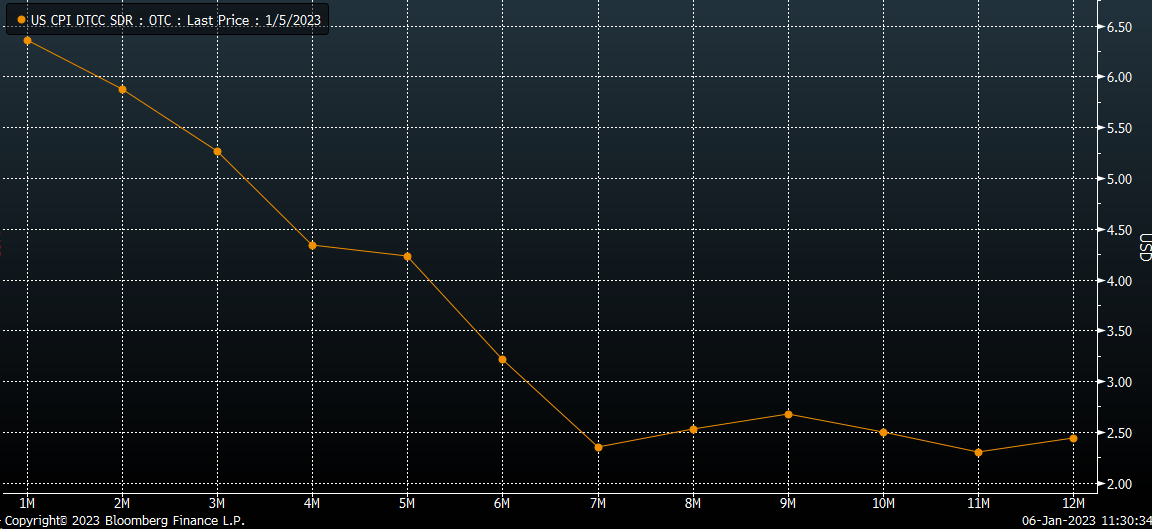

But it also suggests that the Fed is nowhere near cutting rates. Not to mention, inflation rates are still elevated. Based on market expectations, it will take some time to lower inflation rates based on the inflation swap curve, which sees inflation around 2.5% by August, assuming everything goes as planned.

{kind=link}

Bloomberg

Again, the problem is that if inflation does come down as the swaps market implies, it also means that S&P 500 revenue growth will slow dramatically. S&P 500 revenue growth rates change along with the inflation rate over time.

{kind=link}

Bloomberg

So while the market cheers news that the ISM services index crashed in December and inflation rates are coming down, the stock market may not entirely understand what it is that is cheering for. What’s clear is that the Fed is going to be keeping rates to just over 5%, and by the time inflation reaches the Fed target at a minimum, S&P 500 sales and earnings estimates will be severely cut.