MicroStockHub

A composite of the leading commodity futures and forwards on the U.S. and the U.K. exchanges moved 4.68% higher in Q4 and 3.83% higher in 2022.

While the base and precious metals led the asset class higher in Q4, energy and animal proteins posted double-digit percentage gains in 2022.

Nickel, silver, platinum, tin, and lead were the leaders in Q4, with over 20% gains. In Q4, fourteen commodities posted over 10% gains, while nine were over 10% lower. Coal, natural gas, and coffee led the way on the downside in 2022’s final quarter.

Eighteen commodities moved over 10% higher from the closing levels on December 31, 2021, as of December 30, 2022. Eleven raw materials posted double-digit percentage losses. Coal for delivery in Rotterdam, the Netherlands, nickel, heating oil, and frozen concentrated orange juice posted over 20% gains in 2022, while lumber, oats, tin, the Baltic Dry Index, coffee, and cotton moved over 20% lower last year.

As we head into 2023, inflation, supply-side concerns caused by the ongoing war in Ukraine, the rising potential for a U.S. recession, the bifurcation of the world’s nuclear powers, China’s economy, and the unknown will determine the path of least resistance of raw material prices. Meanwhile, commodities did a lot better than stocks and bonds in 2022.

The Invesco DB Commodity Index Tracking ETF (DBC) and the iShares S&P GSCI Commodity-Indexed Trust ETF (NYSEARCA:GSG) are two of the largest commodity-based products. DBC and GSG outperformed stocks and bonds in 2022 even though interest rates and the U.S. dollar index moved appreciably higher on the year. A strong dollar and rising rates are typically bearish for raw material prices, but 2022 was no ordinary year in markets across all asset classes.

The stock market took a hit in 2022- Stocks and bonds fell, and the dollar index rallied

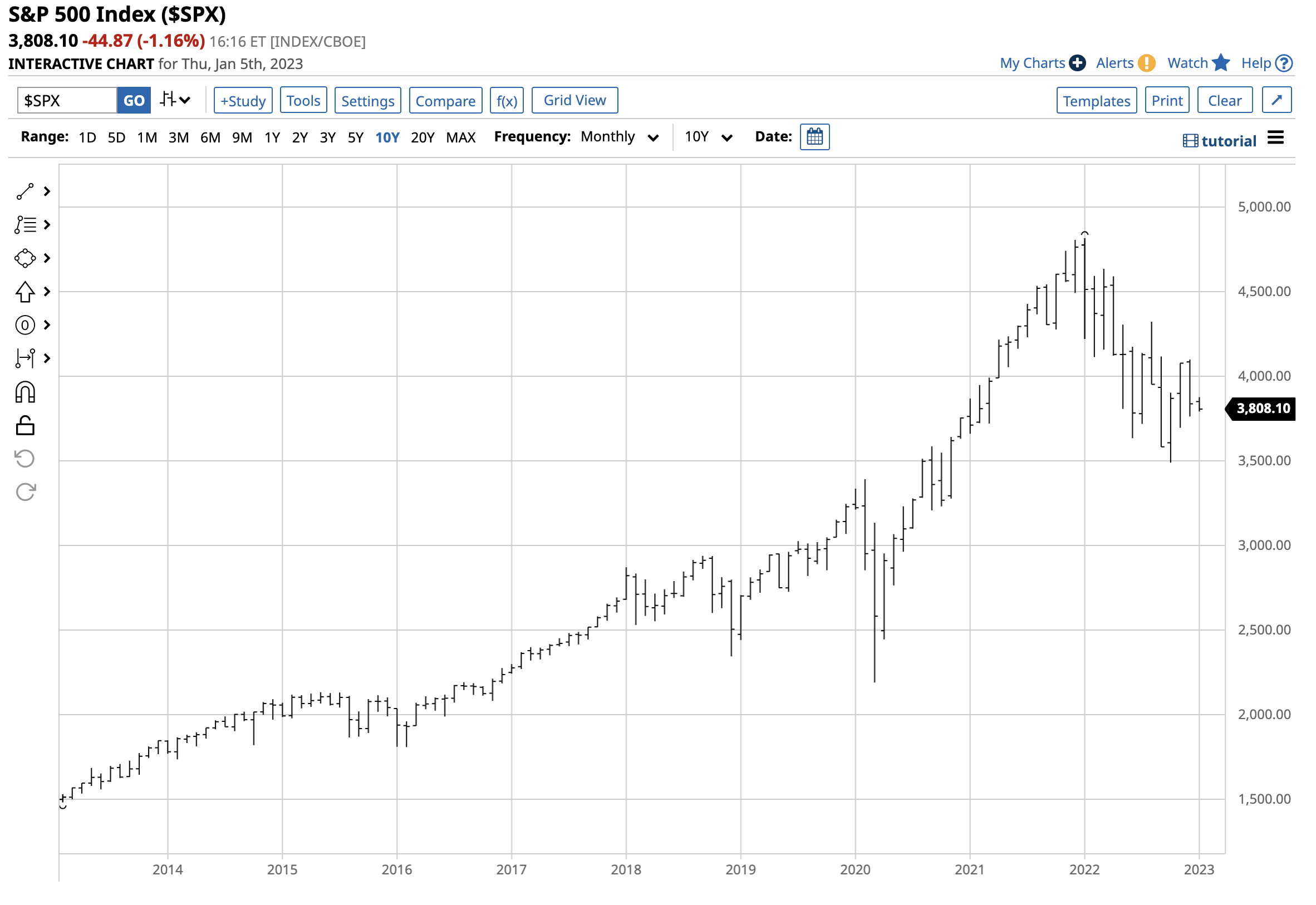

The S&P 500 is the most diversified U.S. stock market index.

Chart of the S&P 500 (Barchart)

{kind=link}

The chart highlights the 19.44% decline in the S&P 500, which was not alone. The Dow Jones Industrial Average fell 8.78% in 2022, and the tech-heavy NASDAQ plunged 33.10% on the year that ended on December 30, 2022.

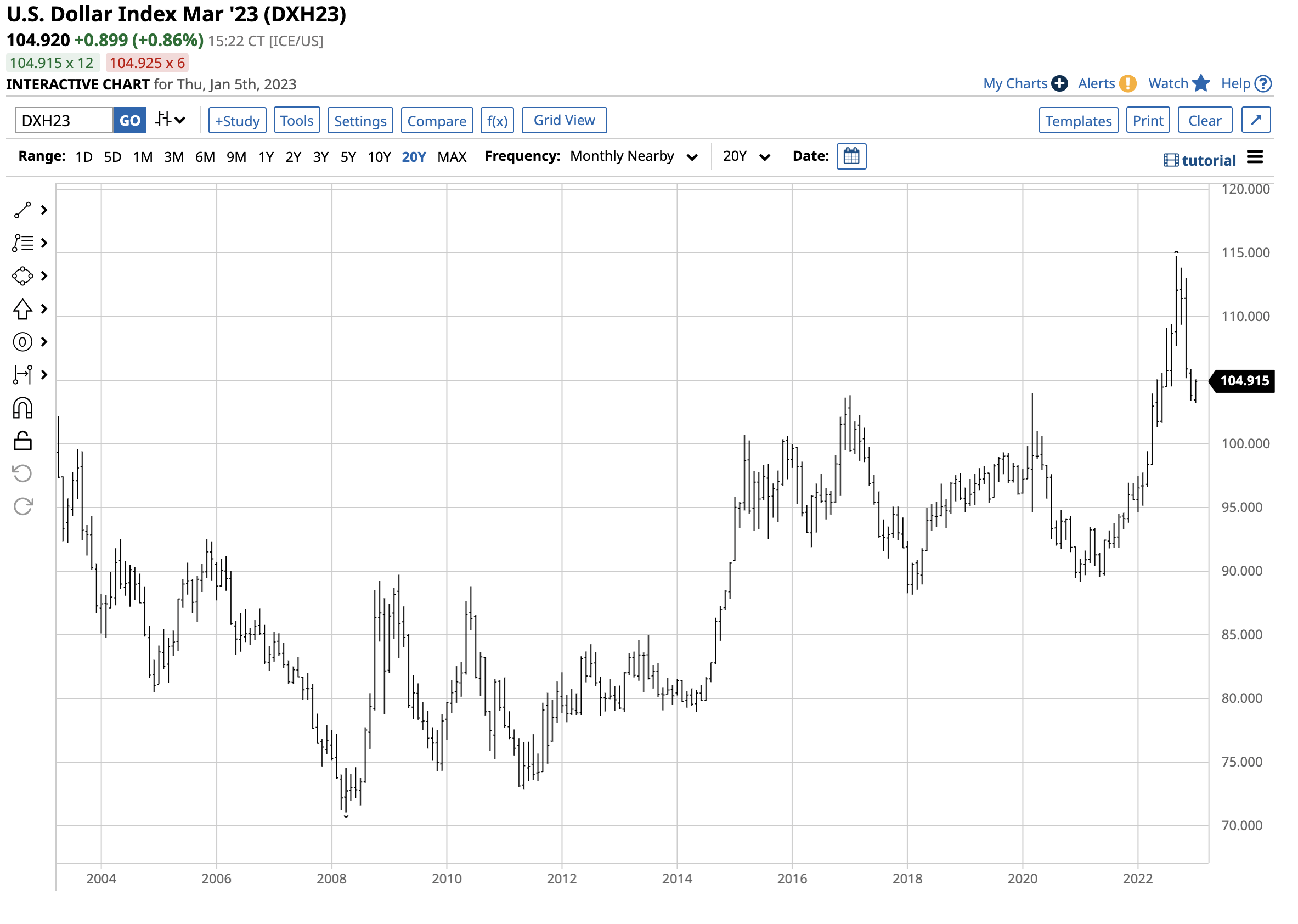

Chart of the U.S. Dollar Index Futures (Barchart)

{kind=link}

The U.S. dollar index, which measures the U.S. currency against other world reserve currencies, rallied 8.03% in 2022. The dollar index settled at the 103.269 level, well below the two-decade 114.745 high reached in September 2022.

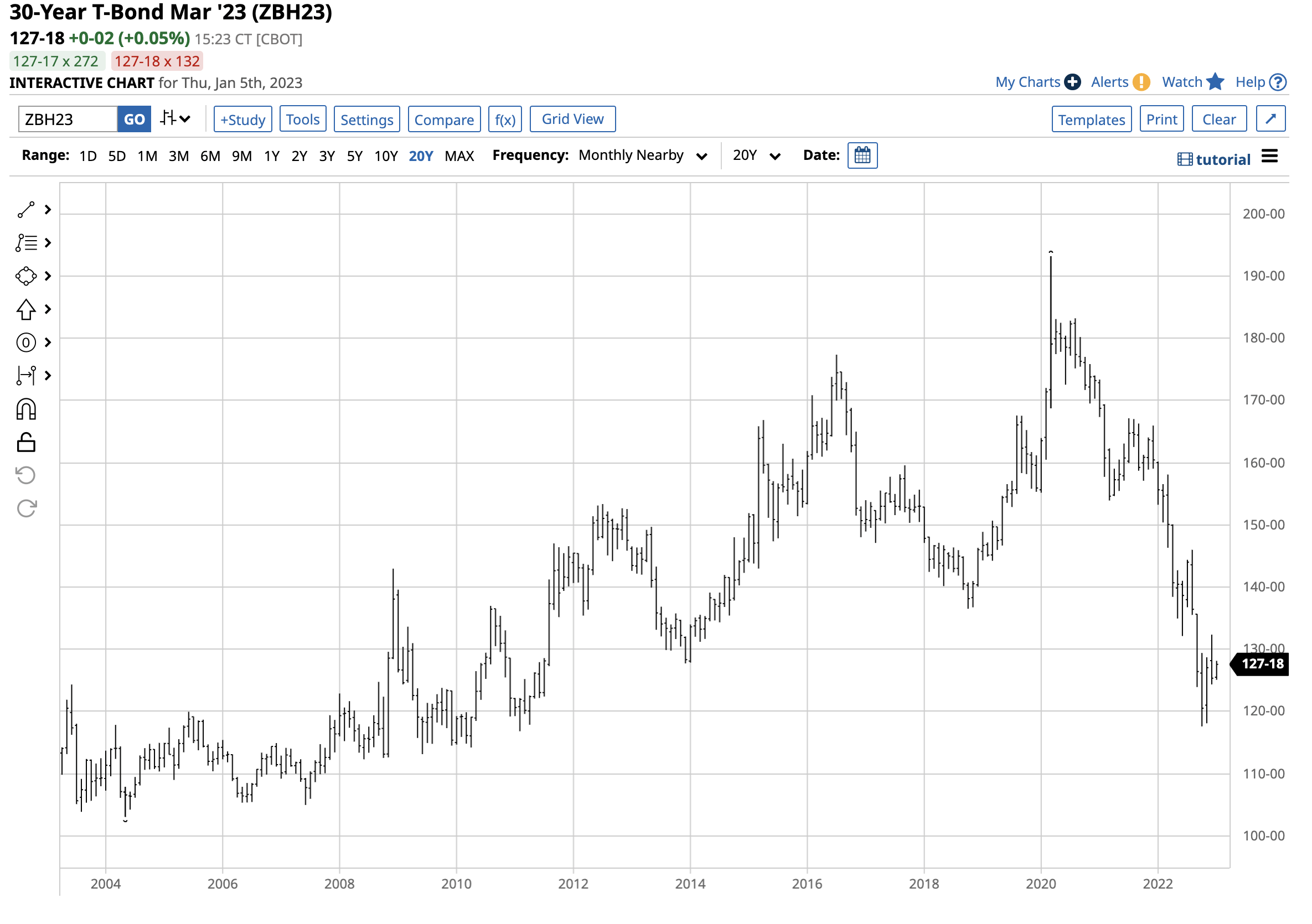

Chart of the U.S. 30-Year Treasury Bond Futures (Barchart)

{kind=link}

The chart illustrates the 21.66% drop in the U.S. 30-Year Treasury bond futures as short, medium, and long-term interest rates moved significantly higher in 2022.

Ordinarily, the risk-off conditions from double-digit stock market losses, a strong dollar, and rising interest rates are a toxic bearish cocktail for commodity prices. However, in 2022, supply-side issues created by the ongoing war in Ukraine, the bifurcation between the world’s nuclear powers, and the highest inflation levels in decades caused raw material prices to rise.

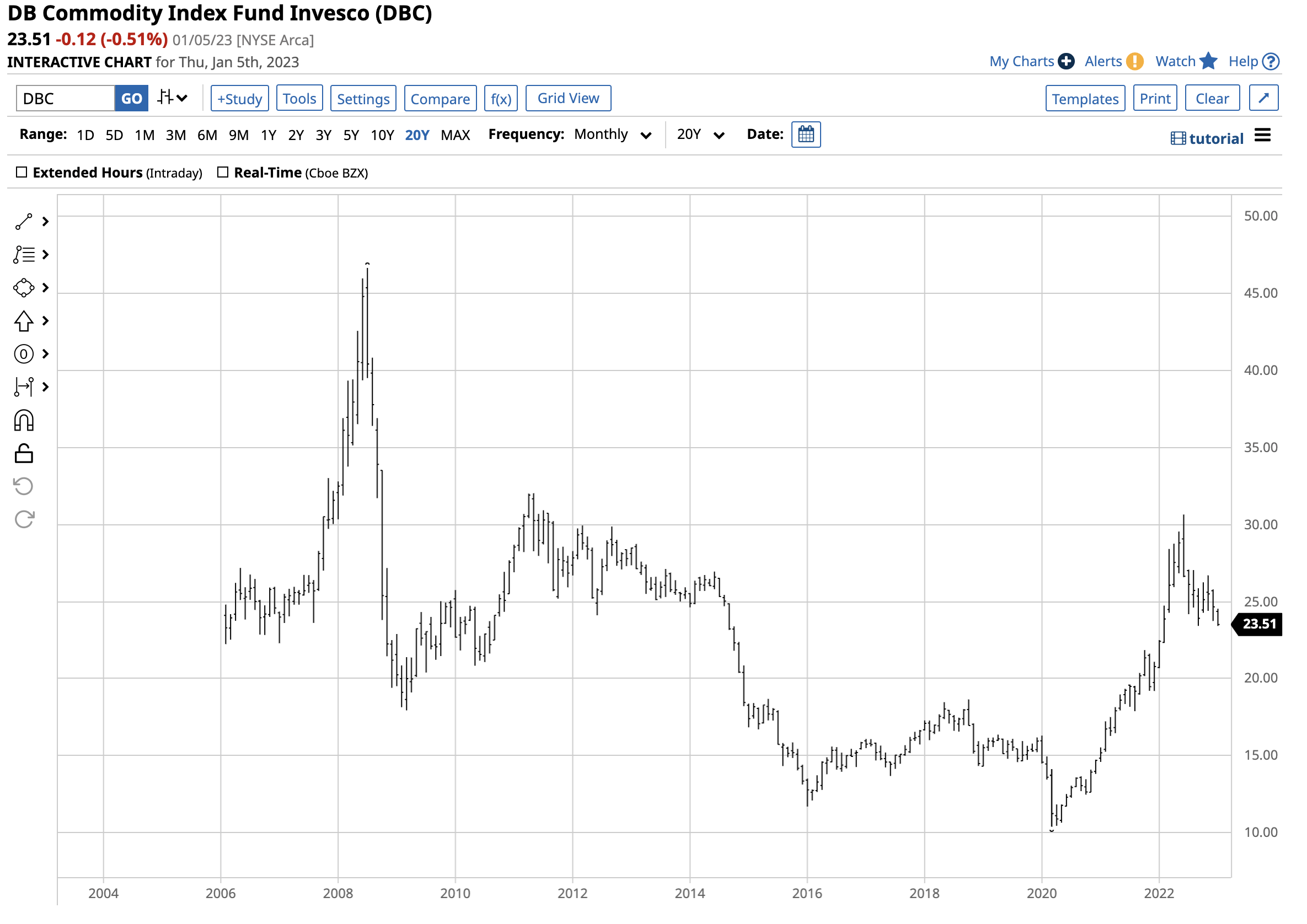

DBC outperformed the leading indices

The Invesco DB Commodity Index Tracking ETF is a highly liquid exchange-traded fund (“ETF”). At the $23.51 level on January 5, DBC had around $2.50 billion in assets under management, trades an average of more than 2.8 million shares daily, and charges a 0.87% management fee.

Chart of the DBC ETF Product (Barchart)

{kind=link}

The chart shows DBC moved from $20.78 on December 31, 2021, to $24.65 per share on December 30, 2022. The 18.6% gain outperformed stocks, bonds, and even the composite of twenty-nine individual commodities that rose 3.83% in 2022.

GSG also did better than the S&P 500, NASDAQ, and DJIA

The iShares S&P GSCI Commodity-Indexed Trust ETF product is another highly liquid ETF. At the $19.86 level on January 6, GSG had around $1.18 billion in assets under management, trades an average of more than 1.65 million shares daily, and charges a 0.75% management fee.

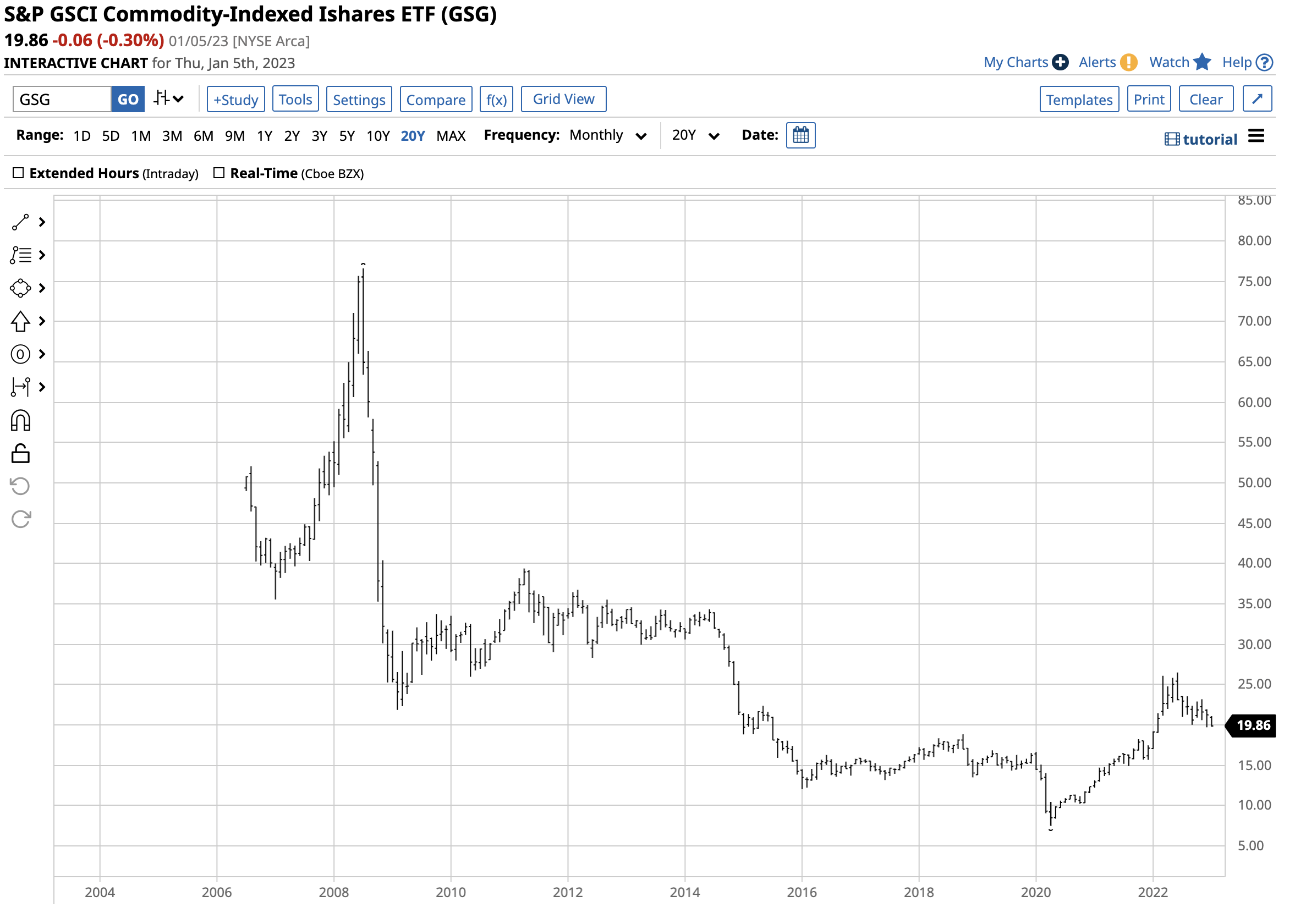

Chart of the GSG ETF Product (Barchart)

{kind=link}

GSG moved from $17.11 on December 31, 2021, to $21.23 per share on December 30, 2022. The 24.1% gain outperformed stocks, bonds, the composite of twenty-nine individual commodities, and the DBC ETF in 2022.

DBC and GSG have significant traditional energy exposures

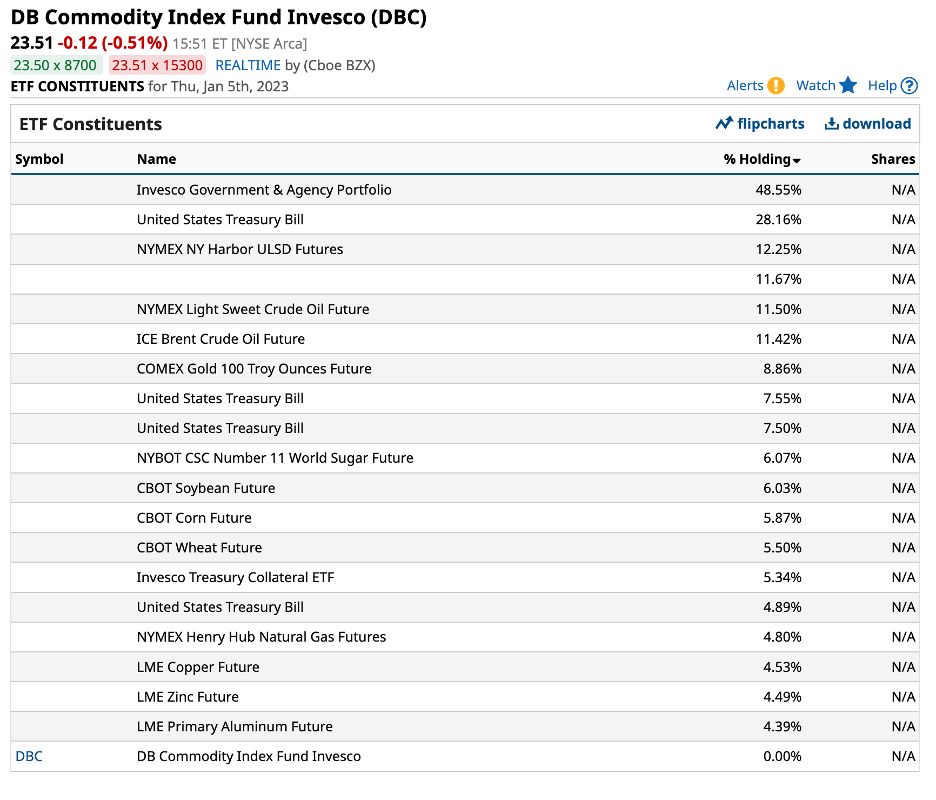

DBC’s top holdings include:

Top Holdings of the DBC ETF Product (Barchart)

{kind=link}

The chart shows around a 40% exposure to traditional energy prices, including crude oil, oil products, and natural gas, as of January 6, 2022. DBC also holds agricultural commodities and metals in its portfolio.

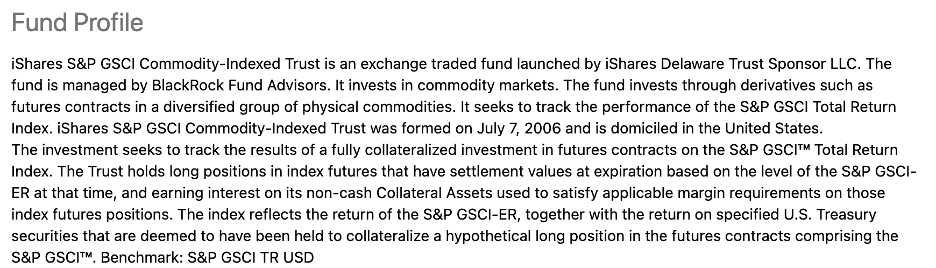

GSG’s top holdings are more elusive, but the fund profile states:

Fund Profile for the GSG ETF Product (Seeking Alpha)

{kind=link}

Given GSG’s outperformance, it is likely the fund managers take a more dynamic approach to its “futures contracts in a diversified group of physical commodities” holdings.

Even though DBC and GSG are weighted in energy commodities, they both outperformed the energy sector balance with oil, oil products, and natural gas, which posted a 15.47% gain in 2022.

The outlook for commodities in 2023

Commodities were the place to be in 2022, and the potential for more gains in 2023 is high. The following factors favor the raw materials asset class this year:

- Many commodities corrected significantly from the 2022 highs, leaving much room for recoveries from the current price levels.

- The trajectory of the Fed’s interest rate hikes will be lower in 2023 than in 2022. Even if the hawkish central bank continues its tightening, short-term rate hikes are unlikely to climb at the same rate as in 2022, when they moved 4.375% higher.

- Inflation remains at the highest level in decades at over the 7% level in the U.S., making short, medium, and long-term real interest rates negative. Flat or negative interest rates are bullish for raw material prices.

- Higher costs increase the production cost for all commodities, from energy to agricultural products and metals to other raw materials. Rising input costs translate to higher prices.

- The ongoing war in Ukraine creates supply-side economic pressures as Russia continues to use food and energy commodities as weapons against “unfriendly” countries supporting Ukraine.

- Energy is a critical component in all business costs, and commodity production is no exception. U.S. energy policy that supports alternative and renewable fuels and inhibits the production and consumption of traditional hydrocarbons translates to more Russian and OPEC control and higher prices.

- The bifurcation of the world’s nuclear powers, with China/Russia and their allies on one side, and the U.S./Europe and their ideological partners on the other, interfere with the worldwide flow of commodities, creating price distortions and supply shortages.

- The green energy initiatives favor base and platinum group metals, where some inventories have been declining to levels that could create shortages. Supplies are likely to struggle to keep pace with the rising demand.

- As China emerges from its COVID-19 protocols and its economy gets back on track, the raw material demand from the world’s most populous country with the second-leading economy will likely soar.

- The declining faith and credit in fiat currencies favor gold and silver, the world’s oldest means of exchange. The aggressive central bank gold purchases in 2022 validate gold’s role in the worldwide financial system and a reason why the metal is likely to rise to new and record nominal highs.

The current commodity bull market began at the March 2020 pandemic-inspired lows. For the reasons stated above, I remain bullish on the asset class for 2023. Meanwhile, bull markets rarely move in straight lines, and commodities are highly volatile assets. I would only buy to add to existing long positions on price weakness, being selective and concentrating on metals, energy, and agricultural products when they are under selling pressure.

My thesis would change if the war in Ukraine ends and a wave of peace descends on the world, which is highly unlikely in early 2023. DBC and GSG were lower than the December 30, 2022, closing prices on January 6. Given the dynamic outperformance, I favor iShares S&P GSCI Commodity-Indexed Trust ETF in 2023.