alberto clemares expósito

The most popular indexes for US investors are the S&P 500 (SPY), the Russell 2000 (IWM), the S&P 600 (NYSEARCA:IJR), and the S&P 400 (NYSEARCA:IJH). The S&P 500 is the most popular index overall, covering roughly 80% of the overall US market cap. The Russell 2000 is the most popular small-cap index. The S&P 600 and S&P 400 are excellent products, but they’re not as widely sold to investors. Of these four indexes, I view the S&P 500 as OK, the Russell 2000 as bad, and the S&P 600 and S&P 400 as good. Here’s why.

Bad: The Russell 2000

Long-running academic research indicates that small-cap stocks tend to outperform large-cap stocks over long time periods. However, the Russell 2000, the main index that investors choose for this strategy, is not the best. The Russell has about 80%-85% market share as the index of choice among small-cap investment products. IWM, the main Russell 2000 fund from iShares, has nearly $50 billion in AUM. It’s very common as the default option for 401(k) investors, but what’s not commonly known is that the index is structurally flawed. This has been heavily reported on by academics, by Seeking Alpha contributor Ploutos, and by the financial press.

There are two main problems with the Russell 2000.

- The annual rebalancing process bleeds tons of money to Wall Street. Each year, the Russell 2000 is mechanically rebalanced to hold 2,000 of the top 3,000 companies in America. Each year, some companies drop out because they shrink to be too small, and some companies graduate to the Russell 1000. This creates an opportunity for hedge funds and proprietary traders to figure out which stocks will be added and deleted from the index funds and buy before the index does, or conversely to sell before the index does. I’ve written about this, calling it the “Great American Small Cap Scam” because hedge funds make billions off of this at the expense of hapless retirement investors. The bigger index funds become, the more of a problem this will become, leading some observers like Michael Burry to call index funds a “bubble.”

- In contrast with other indices, companies are not required to turn a profit to be included in the Russell 2000. Unsurprisingly, including businesses that lose money in the index drags the total return of the index down.

For these reasons, investors should banish any and all index fund products tied to the Russell 2000 from their portfolios.

Better: The S&P 600

The S&P 600 is the better alternative to the Russell 2000. It tracks small caps, currently defined as companies with market caps under a few billion dollars. The most common fund that tracks the S&P 600 is the iShares Small-Cap ETF– ticker IJR.

- The roughly 600 companies in the S&P 600 are chosen by a committee, minimizing the ability of Wall Street to front-run the index.

- To be included in the S&P 600, your company has to make money, introducing a component of “quality” to the index that the Russell lacks.

Rather than tell you about it, I’ll just let you see the difference. Running a quick backtest in Portfolio Visualizer reveals that if you’d invested $10,000 in the S&P 600 since its inception in 2000 and reinvested dividends, you’d have about $75,000. If you’d invested in the Russell 2000, you’d have about $49,000, or ~34% less.

Moreover, the Portfolio Visualizer numbers show that much of the outperformance is concentrated in down markets when low-quality, cash-burning companies tend to flame out. Exactly when you most need to be able to count on your investment portfolio, IJR is a much better choice than IWM.

OK: The S&P 500

The S&P 500 benefits from the same design and profitability criteria as the S&P 600, but has one key drawback, which is a heavy concentration in the world’s largest companies. Small-cap companies have historically outperformed large-cap companies, and this outperformance has been more pronounced when starting your tests from periods when index concentration was particularly high, like the early 2000s.

Index concentration was something I thought about a lot in the earlier days of the pandemic. I felt like the S&P 500 had been usurped by companies like Moderna (MRNA) and Tesla (TSLA) that were added to the index after massive price surges, only to fall back to earth. I also felt that valuations had become rather stretched in mega-cap stocks that were sponges for excess liquidity in the system, whereas smaller stocks tended to trade closer to their fundamental value.

Now that stocks are off 20% from their crazy bull market highs, index concentration is not as severe. But a large valuation gap still persists between smaller stocks and mega caps that you likely would want to hedge against.

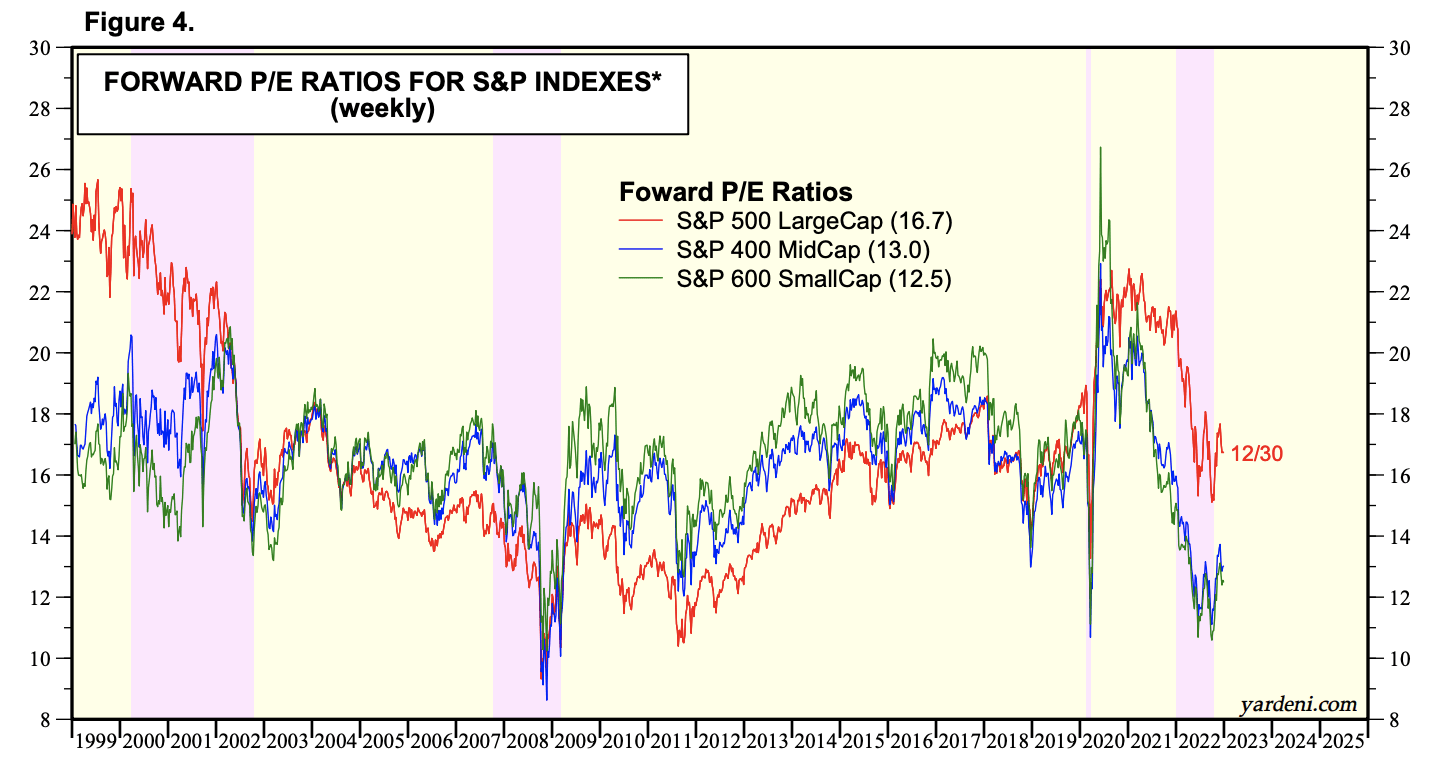

{kind=link}

S&P 500 vs. S&P 600 Valuations (Yardeni Research)

Historically large-cap stocks trade for a lower valuation than small caps most of the time, with the exception of the 1990s tech bubble and the “everything bubble” that started in 2019.

The last time the S&P 500 traded for a big premium to small and mid-caps in 2000, this is what happened.

Small and mid-caps crushed the S&P 500 in the aftermath of the tech bubble as sky-high valuations for mega-cap stocks fell to earth for years. For a deeper dive, take a look in Portfolio Visualizer. Tactically, I think even if you’re a bull, you should try to get away from tech stocks and popular large-cap names trading for 25-30x plus earnings and to small-caps trading for 15x or less.

Better: The S&P 400

The S&P 400 is a great alternative to the S&P 500 because the companies are smaller, but still large enough to benefit from the economies of scale and cheaper financing that seem to have increased profitability for Corporate America in the past decade. The easiest way to invest in the S&P 400 is the iShares Mid-Cap Fund–ticker IJH.

Investing in the S&P 400 allows you to put the S&P 500 inclusion trade in reverse and benefit when companies are promoted to the S&P 500. Some companies get included in the large-cap index because they finally turned profitable, but most get promoted because they’ve grown and their businesses have done well. When this happens, your holdings will be moved to the S&P 500, but you’ll get a higher price for them than you would in a vacuum due to the sheer gravity of S&P 500 AUM pulling prices up. If you’re worried that passive investing may be going too far, IJH is a great way to not only protect yourself from it but possibly even benefit as well.

To this point, IJH and IJR are much closer to pre-pandemic prices than the S&P 500 is. From virtually every angle, the fundamentals simply look better when you look under the hood.

Bottom Line

Investors who are bullish on US equities are likely better off swapping out funds that track the Russell 2000 for funds that track the S&P 600-ticker IJR. Additionally, swapping some S&P 500 holdings for the S&P 400-ticker IJH allows you to sidestep high valuations in the main index while preserving similar upside from economic growth. I’m personally not bullish on US equities this year, but if I were, this is where I would concentrate my exposure. In any case, there should be a substantial long-term advantage from tilting to small caps and quality and away from mega-cap names for investors.